The Tokenomics of Ethereum

Understanding the supply of and demand for Ethereum

Hi friends,

This week I’ll be going into how the economics of Ethereum works. Given the nature of this piece, I’ll add the obvious disclaimer that this isn’t investment advice and please do your own research, etc.

Context

The Ethereum Protocol is one of the largest and most important protocols with a market cap of ~$350B. To understand Ethereum (and to maybe try to gauge the value of an $ETH token :)), it’s important to understand the underlying economics of the token in terms of fees and factors which influence supply and demand. That’s what we’ll discuss today, with a focus on the supply side.

But first, a quick overview of the key stakeholders:

Users: People or Institutions who hold Ethereum either as an investment (passive) or actively to use in DeFi, NFTs, etc

Miners: People or Institutions helping secure the blockchain in return for rewards under the Proof of Work mechanism. Miners incur real costs (in fiat) for electricity/equipment. Note that Miners may be considered users if they hold onto their Ethereum.

Stakers: Users (as defined above) who stake their ETH tokens in order to earn staking fees and help secure the network under the Proof-of-Stake (PoS) mechanism that Ethereum will move to in the future.1

The Current Ethereum Economic Model

Ethereum today operates on a proof-of-work mechanism where miners are responsible for validating transactions and keeping the network secure.

Miners

In order to be incentivized to keep the Ethereum network secure, miners receive two main kinds of fees:

A block subsidy of 2ETH:2 Essentially, the users on the network receive a reward of 2ETH of newly minted Ethereum, which dilutes the exist holders of Ethereum since it increases the number of Ethereum tokens outstanding. This fee is “paid out” at the protocol level.

A priority fee from users: When users transact, they can add an optional tip or priority fee to enable their transaction to be validated more quickly by miners. This fee goes directly to miners from users, and can be quite high during periods of congestion on the network.

These fees help offset the real costs that miners have to incur such as costs of electricity and equipment (powerful computers + cooling, etc.).

Users

When users transact on the Ethereum network, they incur transaction fees, which comprise of two components:

A base fee: Users are quoted a base fee which is dynamic depending on the congestion in the network, which they can either choose to accept (or reject and try to transact later when the fee is lower). The base fee, denominated in ETH, is burned and so reduces the total supply of Ethereum.

An optional priority fee / tip: Users also can optionally add-on a priority fee which goes directly to miners as touched on above and makes it more likely that their transaction has priority in the network and is validated more quickly.

Putting it Together

Now that we know what the token behavior looks like, let’s see how it plays out in terms of supply and demand.

Supply

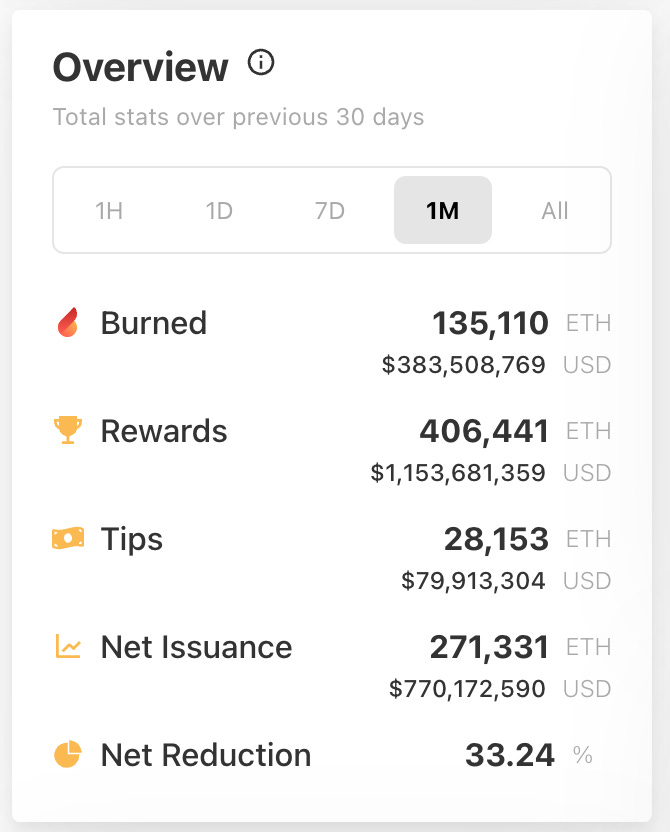

There are currently 118.5M ETH tokens. There are two counteracting forces at work that impact the trajectory of this number.

An increase in supply due to the block subsidy which dilutes all holders (and is like stock-based compensation in a regular company). This number has been fairly steady since the move to EIP-1559 and has been at 13500ETH/day which on an annualized basis is roughly ~4.93M ETH, or 4% of the ~118M currently circulating.

A decrease in supply from the burned transaction base fees (like a stock buyback in a regular company). Since the base fees itself are dynamic and the total volume burned depends on the number of transactions that occur, this number has varied a lot. There was a period where over 15K ETH/day was burned, though currently the number is in the ~4-5K/day range.

The net effect is that roughly 1/3 of the total ETH supply increase is currently being burned, meaning that the net increase in token supply is currently around ~2.7% per year rather than 4% (considering the last month of data).

However, it is important to note that there have been periods where the net issuance on a given day was negative, highlighting the potential deflationary nature of ETH, if used for enough transactions.

Demand

On the demand side, a few things are worth calling out.

The best indicators of demand are the ecosystem metrics such as number of active addresses holding Ethereum and number of transactions, as well as the underlying health of the NFT and DeFi ecosystems. Ultimately, while the ETH token can be viewed as an investment by itself (appreciation) or as a currency needed to participate in a network including NFTs and DeFi, the best long-term gauge of demand is usage of ETH for the latter. While Ethereum saw explosive growth in 2020 and 2021, 2022 has been flat compared to 2021 and the same is true with active wallets (although new wallets have of course joined the network).

Today, since the miners receive ~4% of total ETH supply per year in the form of block rewards, and another ~$1K ETH/day in the form of tips on transactions (0.3% of total ETH supply per year), which they typically need to use to fund their operations, that results in immediate short-term pressure on ETH prices when they sell these earned tokens.

The Future Ethereum Economic Model

Sometime later this year, the Ethereum Mainnet will move to the Proof-of-stake mechanism (technically via a merge with the Beacon Chain of Ethereum) which will i) consume 99.95% less energy and ii) change some of the economics. We’ll dig into the latter for now.

With the shift to Proof-of-stake, holders of Ethereum will be able to stake their Ethereum in order to earn rewards and help validate and secure the network. Unlike mining, this doesn’t need a lot of high-powered computers, and anybody owning or able to pool together 32ETH (needed for a node) can stake their Ethereum. Nodes then have a chance at winning the rewards.

Stakers

Under the Ethereum PoS mechanism, the stakers would receive two types of rewards for helping to secure the network:

Issuance of new tokens: This is comparable to the block subsidy that miners received. However, unlike before when the block subsidy was static, the number of new tokens issued will depend on the number of ETH tokens staked in the ecosystem. The overall issuance will be higher as more ETH is staked, but the return will go down as that happens. The below table shows that even if 100M tokens are staked, the net new issuance is under 2% (issuance rate). It’s important to note that as more tokens get staked, the overall return to the individuals decreases (validator interest).

Tipping Rewards: The stakers will also receive the priority fee or tipping portion of the rewards. While this amount will vary depending on the state of the network and usage, it could further increase the returns to staking. For some context, at today’s levels there are 1K ETH of tipping rewards, which translates to 365K of Ethereum per year. Say 10M Ethereum was staked, that would mean an additional return of 3.65% to the 5.72% above. Note that these returns are denominated in ETH terms, and so by itself aren’t indicative of an implied price in $ terms for ETH.

The upshot is that holders of Ethereum can earn yield potentially in the 8-10% or even higher from ETH rewards they receive depending on:

How many ETH is being staked

The tipping rewards which depend on transaction volume and congestion

Users

Users will still incur transaction fees as in the mechanism today, comprised of two parts:

The base fee which is burned and reduces the total supply of Ethereum

The priority fee or tip which goes to stakers as an additional reward to stake their Eth and secure the network.

Over time, the fees are expected to drop significantly once sharding is implemented, which increases the throughput of the network and allows more transactions to occur from ~50 to ~100K transactions per second over time.

Putting It Together

So what is the upshot of these changes on Supply and Demand of ETH?

Supply

On the supply side, these changes are expected to further slowdown the inflation of Ethereum and potentially actually make it deflationary sustainably.

There will be two counteracting forces on supply:

The issuance of new tokens given as rewards to stakers, expected to be in the 0.5-1% range of outstanding Eth per year but will vary depending on the number of Ethereum staked.

The burning of base fees which can change dramatically depending on transactions, but assuming current levels of ~4-5K/ETH burned may reduce supply by 1.5%. However, a reduction in fees with sharding would mean that many more transactions would be needed to maintain the same level of burn.

Overall, the supply of Eth is likely to move in the + or - 0.5% range per year, although it could deflate much more if transaction volume picks up. Overall, one would expect initially it to continue to inflate, and then perhaps start to deflate as volumes pick up with reduced fees.

Demand

On the demand side, with transaction fees are expected to go down significantly, both with the increasing prevalence of L2s (unrelated to the shift) and sharding (enabled by the shift to PoS), there is expected to be an increase in the number of transactions happening and users coming into the ecosystem.

One important point to note is that now the ETH rewards go to long-term holders of Ethereum who have locked up their ETH. Earlier, there was an immediate downward pressure on demand with miners wanting to sell their rewards. This shift should reduce the downward selling pressure on ETH since the long-term holders may not want to sell their rewards immediately.

Additionally, since the staked ETH gets locked up, this reduces the amount of ETH that is available to be used.

Already today, about 40M ETH is locked up across the DeFi ecosystem as below.

Similarly, already 10M ETH has been staked on the ETH 2.0 smart contract. Once the migration is complete, that number will likely go up, depending on the yields available at the time. In some sense, the DeFi yields available will start to compete with the ETH staking yields available since ETH holders can choose where to deploy their ETH asset.

If the ETH staked goes to 30-40M ETH, and with 40M ETH locked in Defi, that implies that 70-80M out of ~115-120M ETH may be locked up, meaning only ~40M ETH of Supply will be truly available.

Given other use cases of ETH and the need for ETH to continue to participate in things like NFT, that will mean that everyone that needs ETH to participate in this ecosystem will be “competing” over the remaining 40-50M ETH.

As long as demand for ETH continues and people continue to need ETH for DeFi, NFT and other things, that should exert upward pressure on prices. Overall, with lower transaction prices, that is likely to help ETH maintain and grow its use in new experiences and ecosystems over competing L1s.

However, it is worth noting that one obvious risk is the growth of L2 chains which might reduce the need for ETH in that Ethereum functions as the chain of chains that transactions are recorded to.

Closing Thoughts

The move from PoW to PoS should further improve Ethereum’s tokenomics by reducing supply growth and aligning the rewards and incentives to long-term holders of Ethereum who have staked/locked up their Ethereum.

It also allows holders to more directly consider ETH as a yield generating asset (via staking) which may attract even more institutional interest given the 8-10% ETH denominated yields available, which is a return comparable to stock market (ignoring movement in ETH price relative to USD which could swing it to be more or less favorable).

Additionally, lower fees should lead to more use cases and more people and transactions occurring (although Layer 2 chains could pose a risk to this since although more transactions happen, they might occur on L2 chains and be aggregated onto the Ethereum mainnet).

When you combine this with the fact that supply growth slows down and many ETH tokens will be locked up in DeFi or Staked, that means we may have more and more Demand for ETH competing for fewer and fewer available ETH.

Additional Reading

Some additional links I recommend on this topic:

DCF model for Ethereum by Coinstack (which I don’t fully agree with since it converts ETH denominated rewards into $ at current prices to calculate the $ value of ETH but is interesting) and The Investment Case for Ethereum

Stakers by definition have to be holders of Ethereum and so are Users as I’ve defined it.

They also receive Uncle Rewards, but in practice those are small today, so we can ignore them.