A few themes for 2023

The obligatory predictions piece

This is a weekly newsletter about the business of the technology industry. To receive Tanay’s Newsletter in your inbox, subscribe here for free:

Hi friends,

This is a bit late since we’re over a week into 2023 but I figured I’d share a few themes I’m going to be paying attention to this year along with some predictions. These are primarily focused on technology and startups rather than the broader economy though I discuss a few around general consumer behavior at the end.

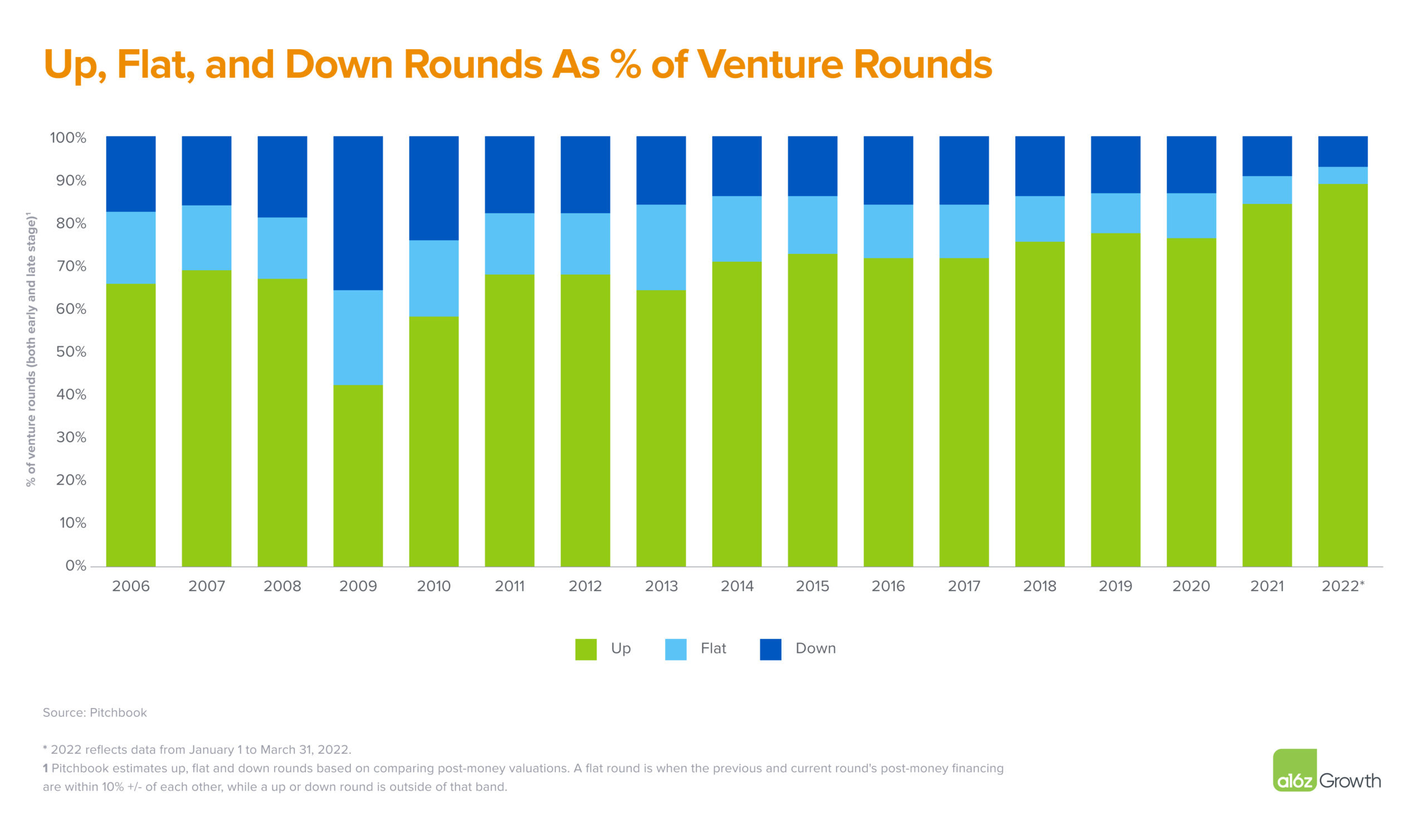

I. Down rounds and structured rounds for startups become more common

Down-rounds (i.e., raising money at a lower valuation than the previous round’s valuation) for private companies have been relatively rare over the past ~3-5 years given the bull market and are somewhat stigmatized. However, given the shift in the market and the fundraising environment currently, many companies (especially beyond Series A) that absolutely need to raise money this year will potentially face no other choice but to accept a lower valuation.

The other alternative that many founders may face is term sheet’s that come with some kind of structure on them. The structure may come in the form of:

participating liquidity preferences or >1x liquidity preferences

additional warrants for the investors (sometimes penny warrants)

debt which converts to equity at IPO

anti-dilution clauses

The purpose of the structure is to essentially include provisions that increase the returns for the investor, especially in specific scenarios, in some sense to compensate for the “high” valuation.

We’ve already seen both of these starting to take place in 2022:

Klarna famously raised a down round at an 85% lower valuation in June ($45.6B → $6.5B)

Snyk raised a ~$200M Series G in a down round at a 13% lower valuation than their 530M Series F.

Companies such as TripActions and Komodo Health have raised structured equity rounds in the 100s of millions from Coatue (which has also raised a ~$2B structured equity fund given the market conditions) .

In 2023, I expect rounds of both types to increase. While structured rounds can seem more attractive to founders because the headline valuation number remains high, I also hope that we’ll see down rounds more normalized so that founders aren’t forced into onerous structural rounds just to maintain a flat valuation. While the decision does vary depending on the circumstances, I think in most cases, founders are setting themselves up better for long-term success by opting for clean term-sheets, even with lower valuation numbers.

II. Generative AI continues to explode

Generative AI has been the talk of the town among tech circles, with products like ChatGPT garnering 1M users in just 5 days and every second company being formed today having Generative AI in their pitch deck.1

But Generative AI is far from mainstream today. In 2023, I expect two things to happen:

A. Generative AI continues to be a very hot sector to invest in.

Lots of money rushes into Generative AI startups, some of which will create outsized returns, but many companies funded will fail because of a lack of a moat or any real differentiation, either being supplanted by the model providers or the companies that have the distribution today. In some sense, it may look like a “bubble”, but there will be real value created. This topic likely deserves its own discussion which I’ll do in a future post.

B. Existing incumbent applications and infra providers adopt Generative AI

The horizontal productivity-type applications will adopt Generative AI features in the coming year. So if you think about some of the common set of companies and products that many knowledge workers use in their day that has a sizable number of users: Notion, Slack, Figma, Canva, Facebook Ads, Adobe, Google Sheets/Docs, Google/Bing, Gmail/Outlook, the rest of the Microsoft Suite I expect at least a quarter of them to launch some kind of Generative AI feature/product. Some such as Notion and Microsoft have already announced their plans to and some such as Canva have already launched features, but they’ll get deeper in 2023. These will be important in bringing Generative AI to a larger set of users and increasing the value of it by bringing it to core workflows.

Similarly, I expect at least one of Amazon and Google2 to vastly improve their Serverless GPU offering and/or launch (to a private beta if not fully) a model-as-a-service to provide developers an alternative to OpenAI’s models.

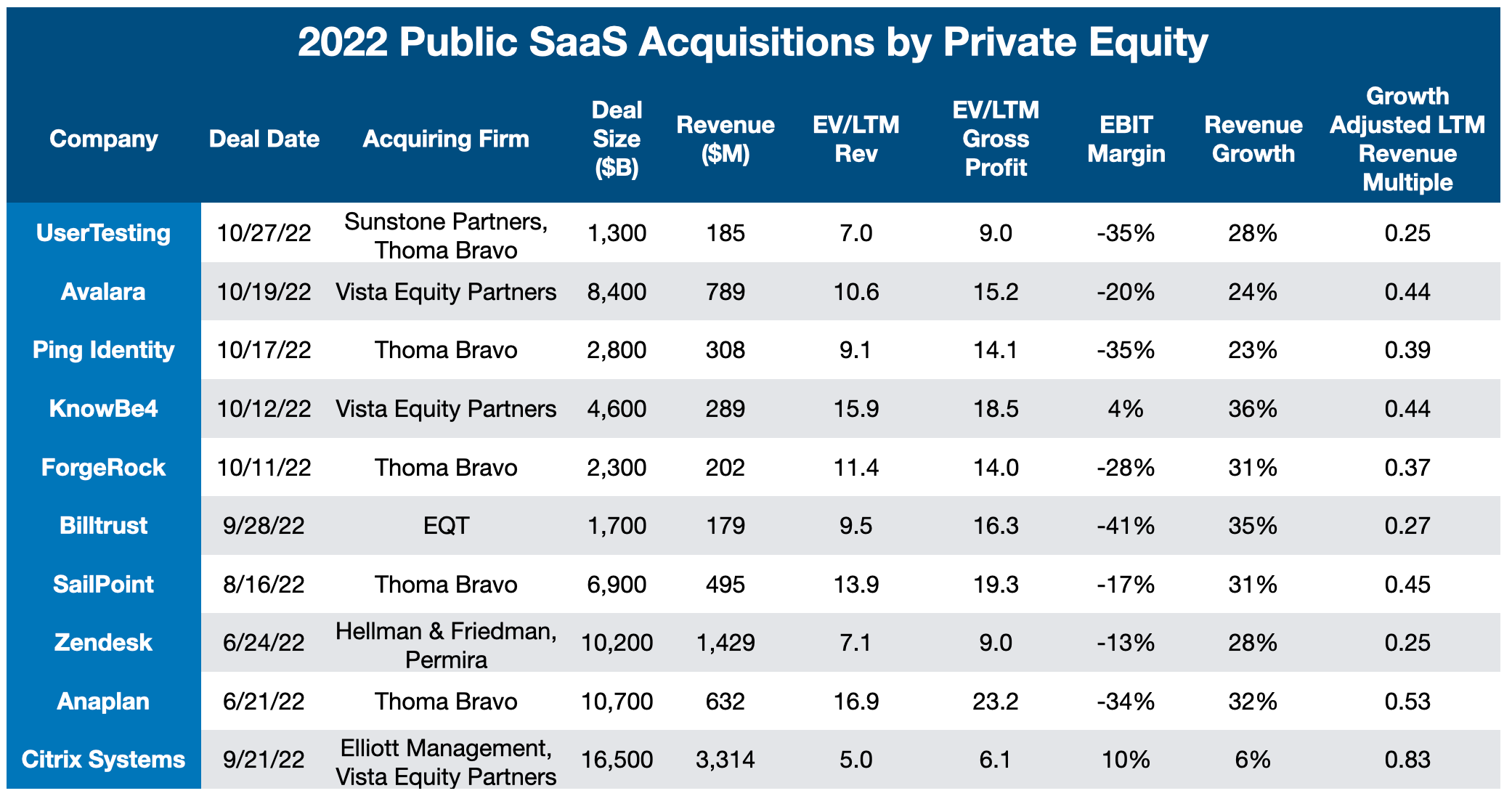

III. Tech PE Acquisitions Galore

In a previous piece, I wrote about how 2022 saw double the transaction volume of Public SaaS companies being taken private by PE firms compared to 2021. I expect the 2023 transaction volume to surpass 2022.

I think we’ll see this trend continue given:

Multiples continue to remain low in SaaS and in tech overall with the Median SaaS EV/NTM revenue multiple currently at 5.3X.

Many companies are getting punished by the markets as they continue to remain unprofitable with high SBC and management teams finding it difficult to pivot from a focus on growth to a focus on profitability

Dry Powder among PE firms continues to remain high at over $1T.

Market fear and incentives of management teams in some cases may be such that an offer at a reasonable premium to current market prices will be accepted.

We’ve already seen Thoma Bravo announce their raise of a $24B fund, the largest technology buyout fund ever raised (coupled with another 8B among two other funds) in December 2022 as a harbinger of this.

If you don’t yet receive Tanay's newsletter in your email inbox, please join the 5,000+ subscribers who do:

IV. It’s time to bundle again in SaaS

Jim Barksdale, the former CEO of Netscape once said:

“There are only two ways to make money in business: bundling and unbundling”

Until mid-last-year, I think we were firmly in the unbundling phase. When money (fundraising) was relatively cheap and growth was the focus, startups and other companies spent money relatively loosely, focusing their software purchases on ease of use, speed, features, etc. Generally, best-of-breed products were purchased in many categories, over say good enough solutions that were cheaper.

Categories such as the data stack, GTM tooling, and Marketing tooling continued to proliferate with many companies using 5-10 pieces of software in each category, and 10s of startups getting funded within each niche within the segment.

Now, I expect much more scrutiny on all kinds of spend across organizations, and a move from companies to reduce their overall software spend. Now couple this with the fact many private companies valued at 100x+ multiples on one product may not be able to achieve the requisite revenue growth to justify the valuation in this software purchasing environment.

What you get is a shift towards bundling, where companies that have become leaders in their categories aim to branch outward to take advantage.

I expect this will play out in a few ways:

Companies that have a foothold in a given product segment will seek to expand their product to move into adjacent markets, often offering these products much cheaper than competitors in the adjacent market. A good example is the likes of Rippling, Deel, Ramp, and others continuing to expand their product suites and encroaching on each other’s turfs.

Companies that are well-positioned in this market will conduct acquisitions to grow their product surface area.

Companies building nice-to-have rather than must-have products with clear ROI will struggle, especially if they’re trying to displace something which is “good enough”.

V. A few more quick-fire ones about consumer behavior

Ozempic (Semaglutide) and Mounjaro (Tirzepatide) become popular for weight loss in the US: These two drugs, typically used by diabetics have shown promising results so far with limited to no side effects (see studies) for weight loss3, and are increasingly being used for them, including by Elon Musk (although the drugs act by suppressing appetite so many regain the weight after using them). I expect usage to continue to grow as more people become aware of them in the US, doctors prescribe them more often, any shortages in supply are resolved and potentially more insurances begin to partially cover the costs for them.

The IHOP of people@ANiMalANPMy diabetic clients can’t get the medications they need because TikTok told folks to use them for weight loss🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃5:53 PM · Dec 23, 202211K Reposts · 95.7K Likes

The IHOP of people@ANiMalANPMy diabetic clients can’t get the medications they need because TikTok told folks to use them for weight loss🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃🙃5:53 PM · Dec 23, 202211K Reposts · 95.7K LikesSide Hustles and Content Creation continue to Grow among Gen Z and Millennials: 2020 and 2021 saw the Great Resignation with workers leaving their jobs to pursue their passions. 2022 saw Gen-Zs popularize the idea of “quiet quitting” or doing the bare minimum at work. In this current economic climate, many people might be hesitant to leave their jobs (and similarly many might not be able to find the right job). But given their need for fulfillment and desire for independence, I expect more and more people to continue to find a side hustle – creating on TikTok/YouTube/Instagram, re-selling sneakers or secondhand clothes, using AI to do various freelance gigs across the internet, starting newsletters/podcasts, etc. While I’m actually bearish on Creator Economy startups, I am bullish on more and more people continuing to create content and find side hustles.

Over 60% of Gen Zers have started a side hustle since the pandemic began, according to a 2021 Bank of America survey.

Consumer Subscription Businesses struggle as consumers reign in spending: A potential recessions plus one of the lowest savings rate ever will likely prompt consumers to reduce their spend, impact consumer subscription businesses. I expect churn to go up and fewer users to upgrade to paid versions, with many opting to potentially downgrade or stick to lower-priced / free versions. I can see this impacting consumer subscription businesses across media and entertainment, fitness, learning, etc.

This is not a precise analysis :)

The other big cloud provider Microsoft is an investor in OpenAI and offers an OpenAI x Azure service

It should go without saying, but I am not a doctor and these drugs are very early, and magic pills tend to not exist so please do your own research.

Thanks for reading! If you liked this post, give it a heart up above to help others find it or share it with your friends.

If you have any comments or thoughts, feel free to tweet at me.

If you’re not a subscriber, you can subscribe for free below. I write about things related to technology and business once a week on Mondays.

Great article, as always. May 2023 to be awesome for you!