Unitree's IPO Filing: The State of the Robotics Market

Profitable hardware, the humanoid shift, vertical integration and a $300M bet on the model layer

I’m Tanay Jaipuria, a partner at Wing and this is a weekly newsletter about the business of the technology industry. To receive Tanay’s Newsletter in your inbox, subscribe here for free:

Hi friends,

Unitree Robotics recently filed for IPO on Shanghai’s STAR Market, looking to raise $620 million. The filing is quite interesting1 because it gives us a good sense of the current state of the robotics market.

Unitree is profitable, growing fast, and has shipped more humanoid robots than anyone else in the world.

In this piece, I’ll discuss:

What Unitree makes

The humanoid flip in revenue mix

Who is buying robots today (and why)

The vertically integrated approach

The financial picture

The model layer ambitions

I. What Unitree Makes

Unitree was founded in 2016 in Hangzhou by Wang Xingxing, a self-taught roboticist who famously built his first quadruped robot in his apartment. The company has 480 employees, roughly 175 in R&D.

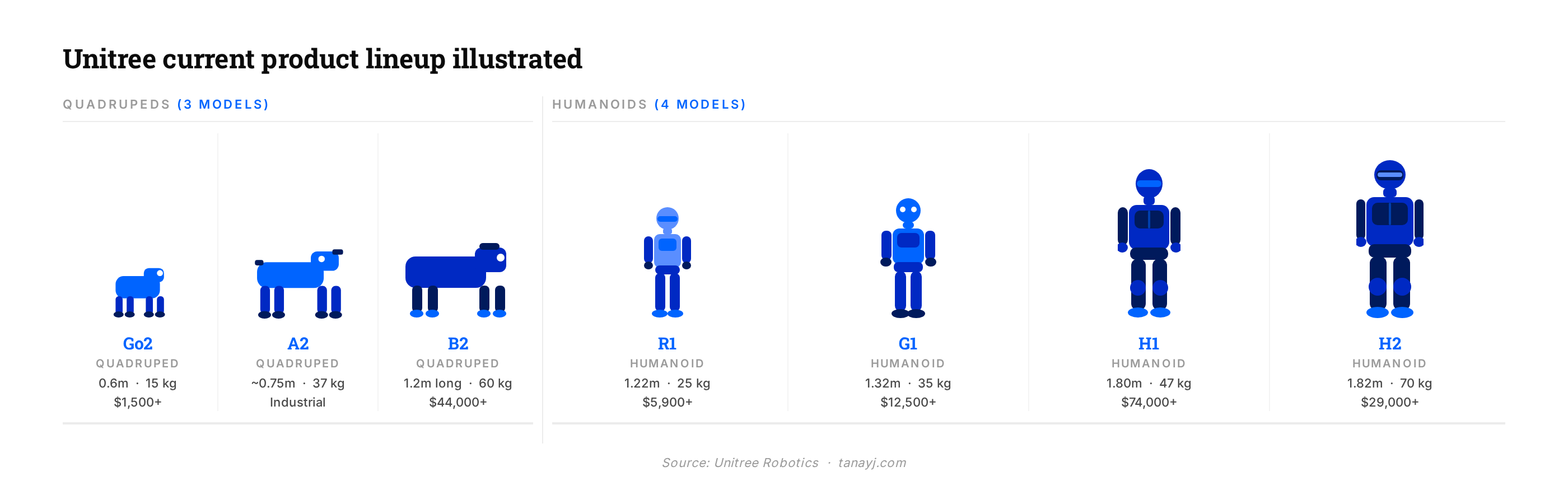

It sells two product lines:

Quadrupeds: the Go2 (consumer and research), B2 (industrial), and A2.

Humanoids: the H1, H2, G1, and R1. The G1 is the one you’ve probably seen in viral videos, standing 1.32 meters tall and weighing 35 kilograms.

The company has been selling internationally since 2018. More than 35% of revenue comes from outside China, including a significant US academic customer base.

II. The Humanoid Flip

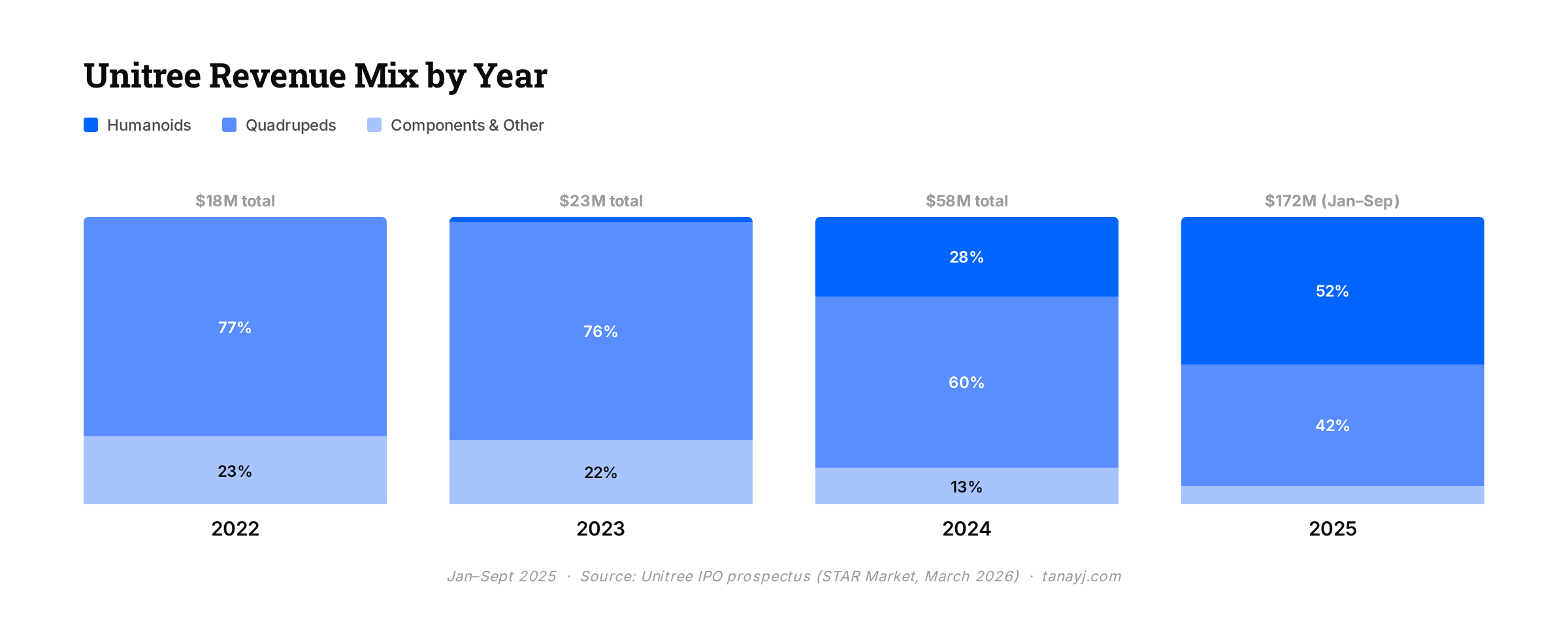

Two years ago, Unitree was basically a robot dog company and was primarily selling quadrupeds. Humanoids represented just 1.9% of its revenue in 2023.

By the first three quarters of 2025, humanoids accounted for over half of core revenue.

What drove it was a combination of product-market fit and aggressive marketing. The company’s humanoids performed at China’s CCTV Spring Festival Gala, one of the most-watched broadcasts in the world, for two consecutive years. Jensen Huang put a Unitree robot on stage at GTC in 2024.

The brand exposure converted into commercial and research demand in a way that most Chinese hardware companies have never really managed.

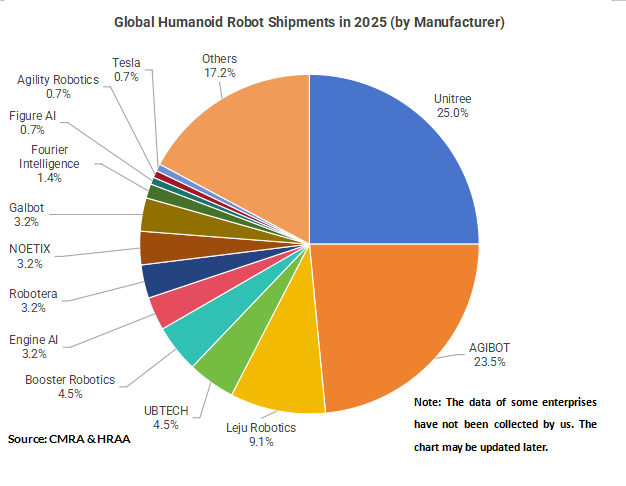

The shipment numbers for humanoids are particularly impressive when compared to others. Unitree shipped roughly 5,500 humanoid units in 2025, making it the largest humanoid maker by volume. AGIBot in China comes closest. As a point of comparison, the numbers for well-known US companies such as Figure AI, Agility Robotics are in the 100s if that

The 5-year target in the prospectus is 75,000 humanoids and 115,000 quadrupeds annually. That’s roughly ~14x the 2025 humanoid volume. It’s ambitious, but also highlights how early we are in the journey.

III. Who Is Actually Buying Robots Today

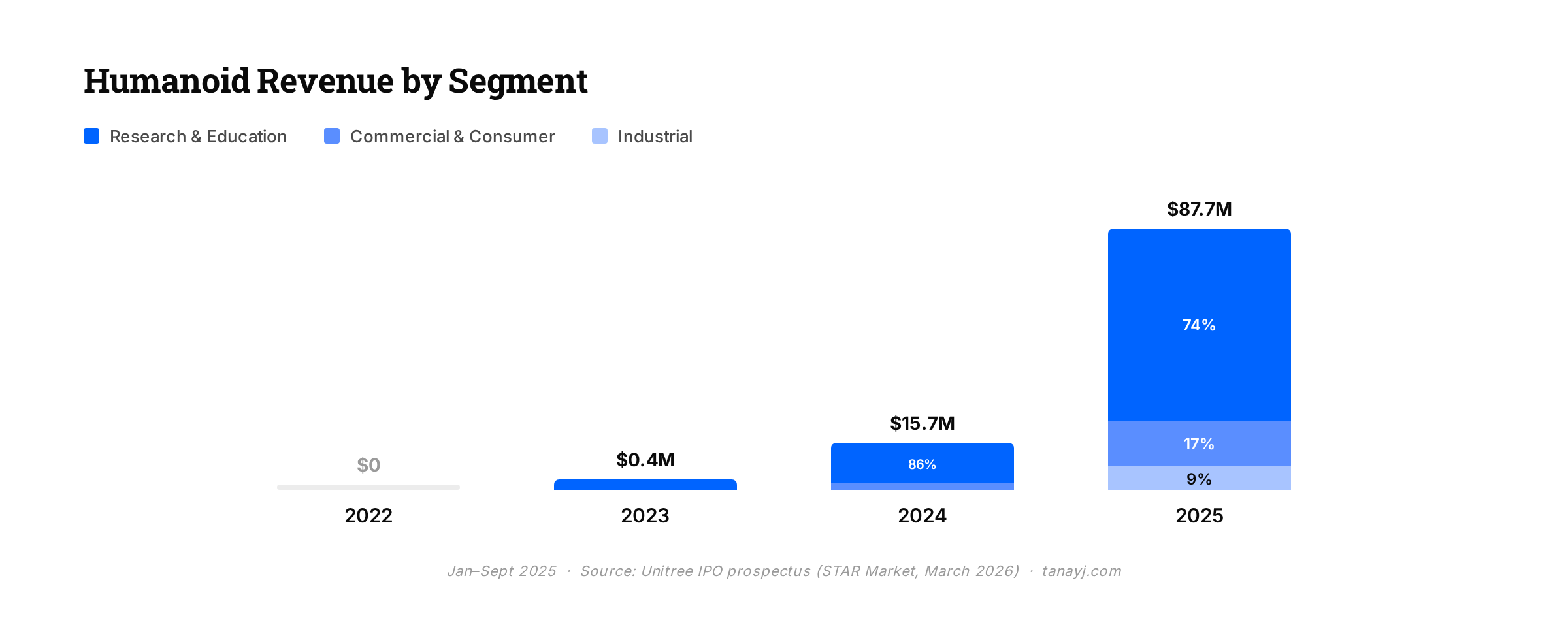

The prospectus breaks down buyers into three categories: research and education, commercial and consumer, and industrial applications.

The stark reality is most humanoid demand is for research and education use cases today.

1/ Research and education accounts for 74% of the revenue/shipments for humanoids. The academic buyer has been Unitree’s anchor since at least 2022 and remains the biggest source of aggregate revenue for the company. Researchers

2/ The commercial and consumer category accounts for 17% of shipments for humanoids. Non-academic consumers who buy these robots are mostly deploying them “for show”: as attractive promoters in retail settings, at tourist sites, in performances and exhibitions. Consumer revenue nearly quadrupled year-over-year in the first nine months of 2025, which sounds impressive until you realize the starting base was quite small. The real-world use case for the $25,000 humanoid robot, today, is apparently standing at the entrance of a store in Shenzhen to attract visitors.

3/ Industrial applications accounts for only 9% of shipments for humanoids. Unitree acknowledges that industrial deployment is more limited because the technology is less mature, highlighting the state of the technology today. Of this 9% of shipments, about 50-70% of it is for use cases like enterprise reception and tour guides, and so in aggregate only 3-4% of humanoid shipments are for things like enterprise reception and inspection.

On the quadrupeds side, things are a bit more promising: only about 1/3 of the revenue is from research, with over 40% from commercial use and the rest from industrial use. There, the productive use cases are more well established. Customers include State Grid, China Southern Power Grid, PetroChina, Sinopec, Baowu Group and JD.com (which is Unitree’s largest customer). These are companies that use the quadrupeds for real inspections of chemical plants, substations, coal mines, pipelines, etc.

If you don’t yet receive Tanay’s newsletter in your email inbox, please join the 10,000+ subscribers who do:

IV. The Vertical Integration Approach

One of the unique aspects of Unitree is that it self-designs and manufactures most of its critical components: high-torque motors, precision reducers, encoders, joint modules, intelligent controllers, high-precision sensors, dexterous hands, LiDAR, and cameras. Actuation (the motors, reducers, and joint systems that actually move a robot) typically represents 40-60% of a humanoid robot’s total bill of materials, according to McKinsey.

Most companies in the space source these externally but Unitree builds them itself. Purchased components represent only about 14-18% of total costs. The only things it outsources are commodity parts such as the battery cells, flash storage and differentiated aspects such as the core compute board.

The per-unit manufacturing cost for a quadruped fell from roughly $3,300 in 2022 to about $1,800 by mid-2025, a 46% drop. Humanoid costs fell too, from about $10,800 to $9,200 over the same period.

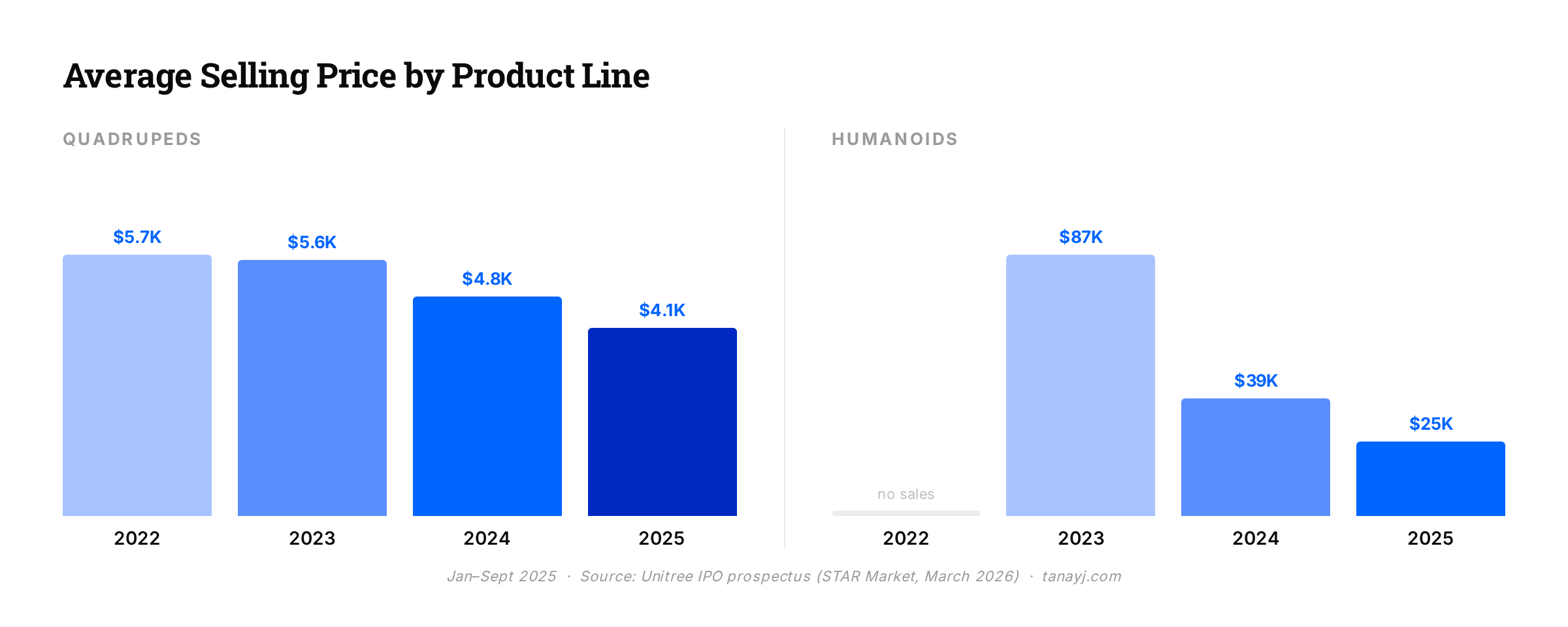

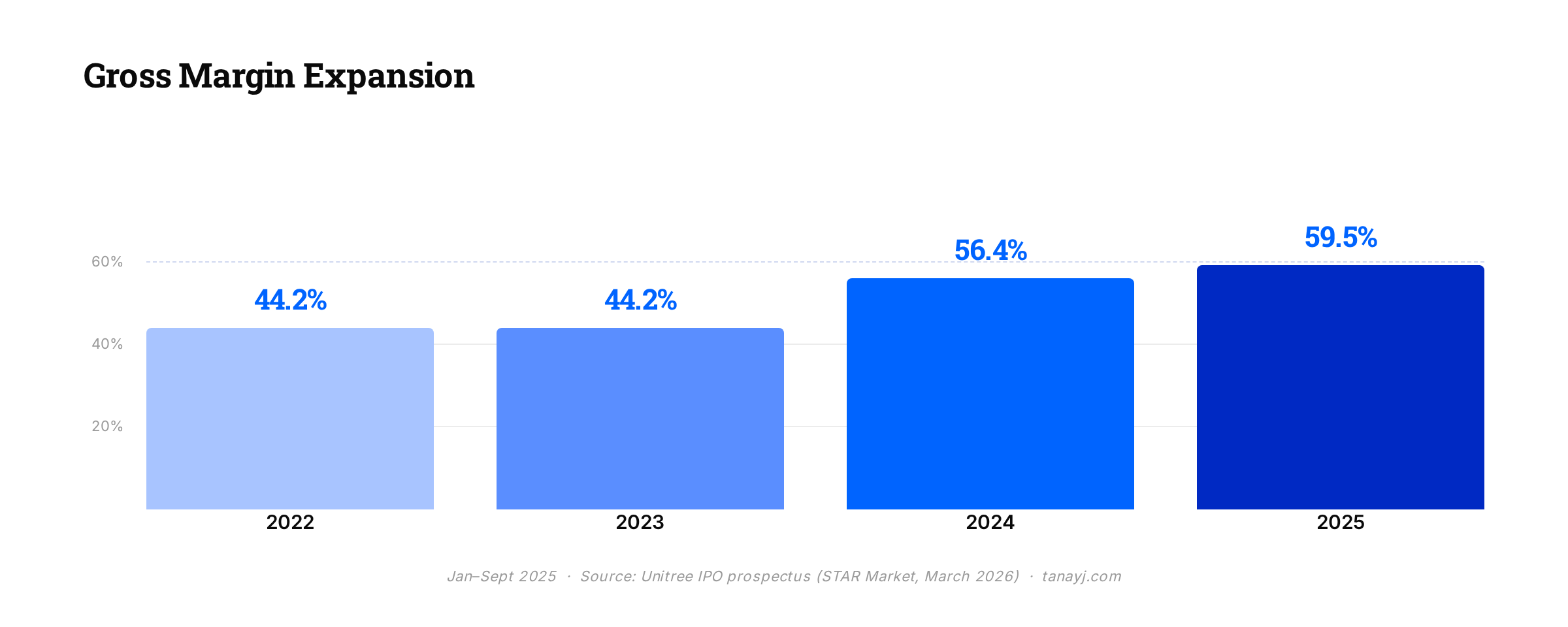

Interestingly, the ASPs of quads and humanoids also fell significantly ever year as the graph below show. And yet gross margin expanded through this entire period, from the mid-40% range in 2022-2023 to nearly 60% in 2025, in big part because of their approach to vertically integrate.

V. The Financial Picture

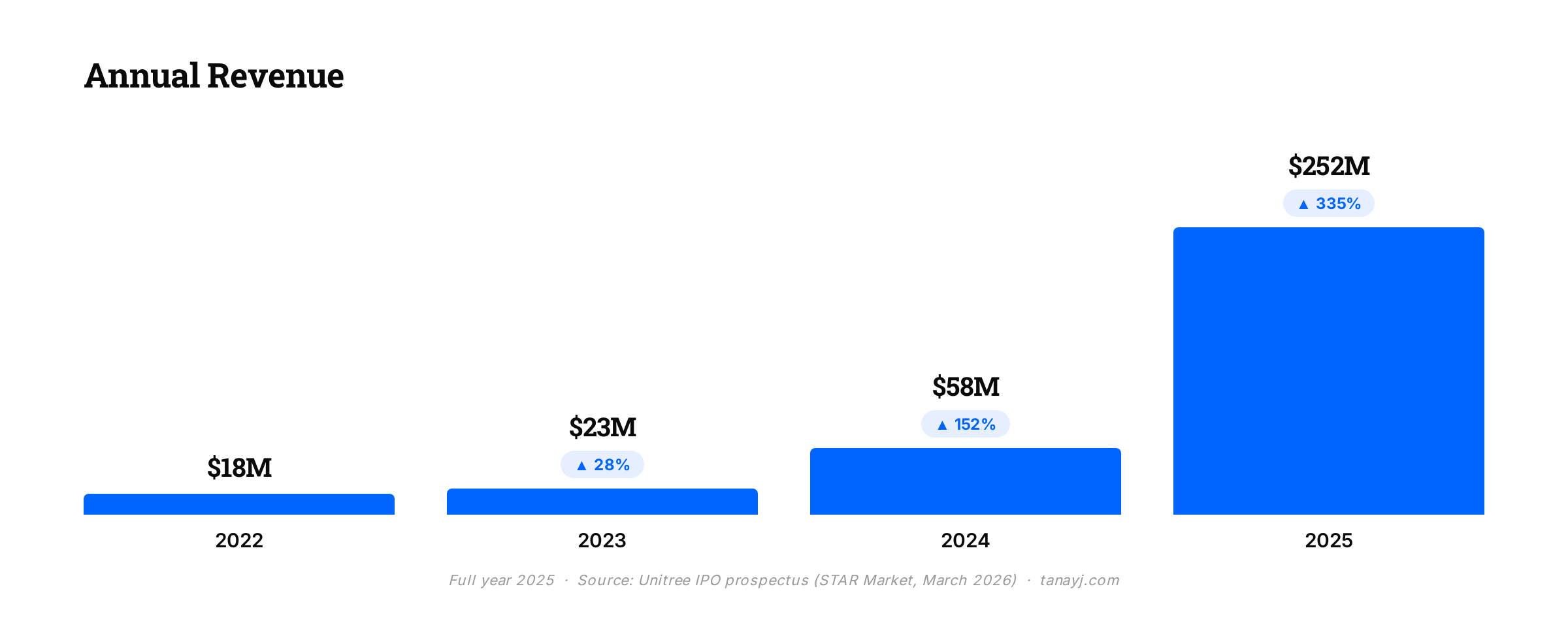

Revenue grew from $58M in 2024 to expected ~$252M in 2025, a 335% jump owing to strength particularly on the humanoid side. International sales represented more than 55% of revenue for most of the company’s history. In 2025, domestic China overtook exports for the first time, though absolute export revenue still more than doubled year-over-year.

Gross margins are nearly 60% and have expanded over the years as below.

To put those margins in context: most hardware companies run 30-40% gross margins. Software companies often hit 70-80%. Unitree is relatively high for a company selling physical robots owing to their vertically integrated approach and the relatively differentiated products today.

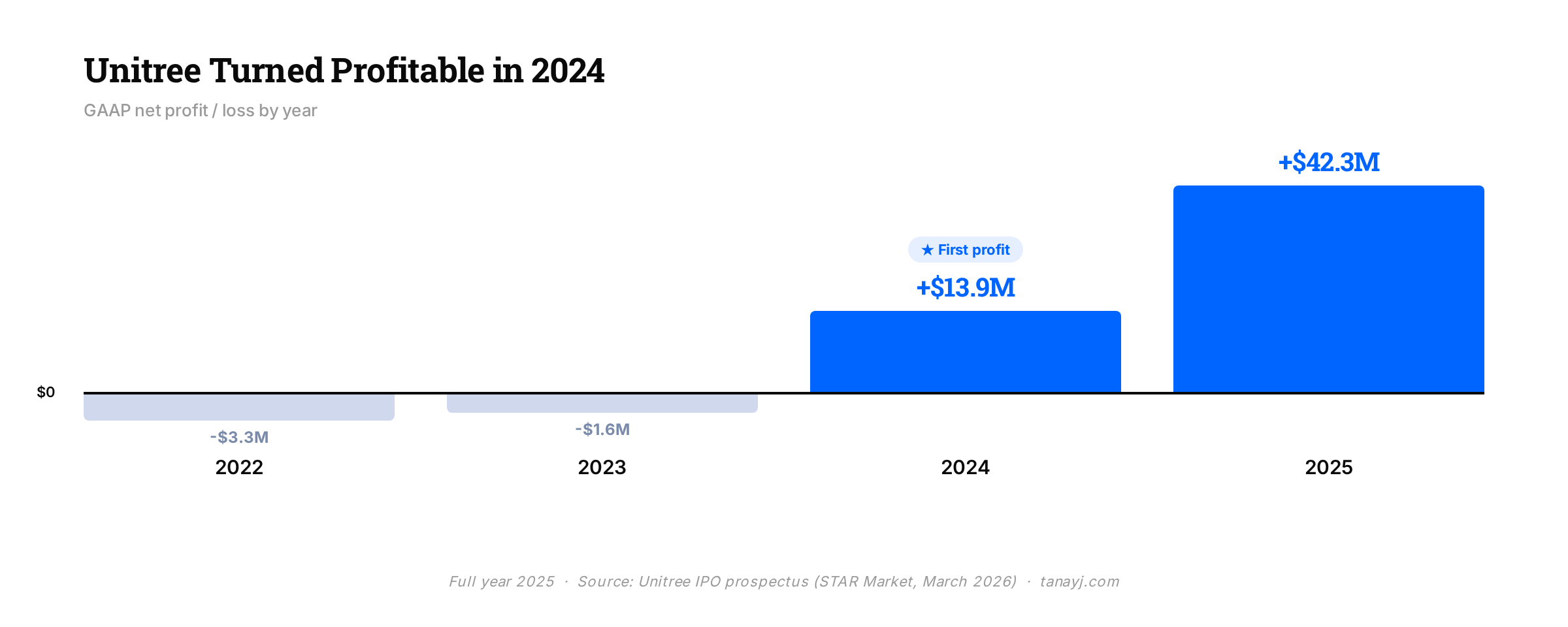

The company turned profitable in 2024 on a GAAP basis and will have margins of around 18% or closer to 35% on an adjusted basis.

Unitree is targeting a ~$6-7B valuation at IPO.

VI. Model Layer Ambitions

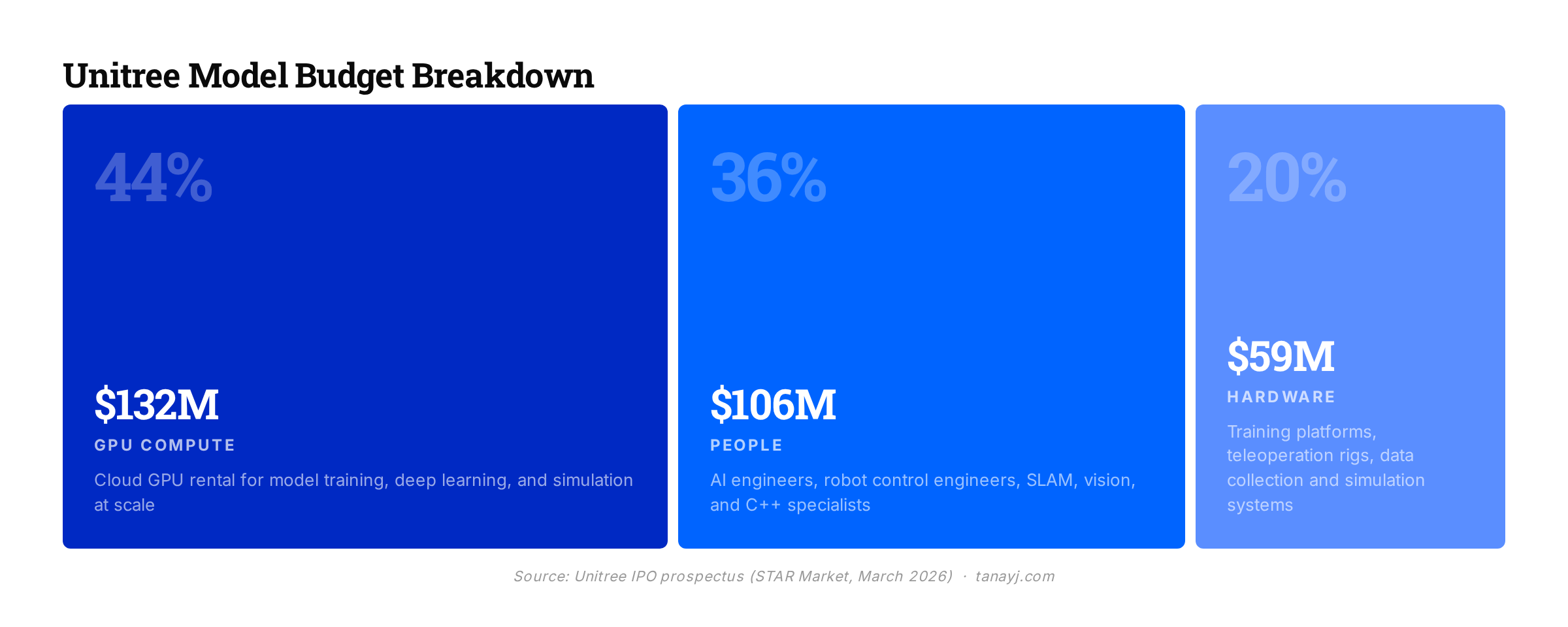

Unitree is planning to spend nearly half the IPO proceeds on software. Of the $620M raise, roughly $300M is earmarked for AI model training over the next three years, about $100M per year devoted to what the company calls its “Embodied Large Model”.

The prospectus describes two parallel model architectures. The first is VLA (Vision-Language-Action): a model that maps directly from visual and language inputs to motor commands, letting robots generalize across unfamiliar tasks without hand-coded instructions. The second is WMA (World Model + Action), which they describe as their higher-conviction bet. A WMA model builds an internal simulation of physical reality. The robot predicts what will happen before it acts, rather than learning purely through trial and error.

They’ve shipped initial versions of both. In September 2025 they open-sourced UnifoLM-WMA-0; in January 2026, UnifoLM-VLA-0.

They also detailed the rough breakdown of spend towards the model, which is below:

Unitree’s hardware lead is real today, but the company understands that durable advantage in robotics probably requires owning the model layer too: the system that decides what the robot does and how it moves. The software ambition also makes sense as a hedge against commoditization. Unitree built its moat in hardware manufacturing.

But if actuators and joint modules eventually become standard parts, like batteries in EVs, the model layer is where the defensibility shifts to.

VII. Closing Thoughts

Unitree has a profitable hardware business, a real manufacturing moat, and more humanoid volume than anyone else at a price point others can’t touch. But the broad commercial adoption story is still in its early chapters as highlighted by how the humanoids are actually used. The “for show” use cases dominate consumer demand and Industrial deployment is narrow.

Unitree gives a glimpse of where the robotics market is currently with a lot more to come on the model side, hardware side and use cases side. If you’re building in the robotics and embodied AI space, feel free to reach out at tanay at wing.vc.

Despite being hard to read because it wasn’t available in English, but luckily Claude and ChatGPT were able to translate.