Inside the Largest IPO Ever: Breaking Down the SpaceX S-1

Why Starship, Starlink, and xAI belong under the same roof, and where they're headed

I’m Tanay Jaipuria, a partner at Wing and this is a weekly newsletter about the business of the technology industry. To receive Tanay’s Newsletter in your inbox, subscribe here for free:

Hi friends,

SpaceX filed its S-1 this week, ahead of what will likely be the largest IPO ever (~$75B raised at a reported $1.75T valuation).

SpaceX is a unique and inspiring company. It’s not often you see a mission statement on an S-1 include “to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars”.

SpaceX on the face of it is three companies combined together: a rocket launch business, a satellite internet business, and an AI lab (after the xAI merger). But the way I’ve come to think about SpaceX (or at least how SpaceX wants to be thought of) after reading the filing is less as a rocket company with an AI lab attached, and more as the physical infrastructure layer for the AI and space economy. I’ll walk through how the three businesses work today, and how they could be far more connected in the future than they look.

In this piece, I’ll cover:

SpaceX’s three segments today

The two deals that change the AI story

What the financials look like played forward

Orbital compute and the Space economy

The Starship Bet

Musk’s pay package, gated on a Mars colony and data centers in space

I. Understanding SpaceX today

SpaceX reports in three segments: Space, Connectivity, and AI. They’re wildly different businesses on one balance sheet, so it’s worth taking each on its own.

Connectivity is the star today, growing fast and very profitable, essentially helping fund the rest. Space looks like a loser on operating income but is actually EBITDA-positive once you add back the Starship R&D and depreciation. AI is a deep loss on every line but more on that later.

A. Space

SpaceX was founded in 2002. The early history may be familiar to some: Falcon 1 reached orbit in 2008 (the first privately built liquid-fueled rocket to do so), they landed a booster back on Earth in December 2015, and by 2017 they were routinely reusing Falcon 9 boosters. Reusability has been key to the rest.

It dropped SpaceX’s launch cost to about $2,700 per kilogram, roughly 85% below the historical industry average of $18,500, and that cost collapse is what made everything downstream possible.

SpaceX began as an external launch provider. The early customers were NASA (Commercial Resupply from 2008, then crew), commercial satellite operators, and the Pentagon, and those contracts funded the company for its first decade and a half. Starlink only started launching in 2019. So the business was built on outside demand, and then internal Starlink deployment grew on top of it until it became the majority of flights.

SpaceX flew 96 Falcon launches in 2023, 134 in 2024, and 165 in 2025. But most of those weren’t for paying customers. Customer launches were 33, 45, and 43. The rest (63, 89, then 122) were internal: mostly Starlink deployments and some development tests.

The chart below highlights this shift. The launch business is now overwhelmingly SpaceX flying for itself, and the internal share keeps climbing (74% of launches in 2025, up from 66% in 2023).

They built a launch business for other customers and used the same capability to deploy their own constellation. The launch business and capability is the railroad of sorts that made everything else possible.

Still, the Space business makes over $4B in revenue for external launches. While some of that is government development contracts that aren’t tied to specific launches, one rough proxy is that at 43 external launches in 2025, each launch is worth about $95M in revenue to them. But the thing to note is that for internal launches that deploy Starlink, SpaceX doesn’t book any Space-segment revenue. It capitalizes the launch cost inside the Connectivity segment and depreciates it over time. So Space-segment revenue only reflects the revenue from the ~1/4 of launches which are external.

The filing notes this: despite a rising launch cadence, Space has “relatively lower revenue scale and revenue growth” because its results don’t reflect the internal launches that are the foundation of the company.

Financially, Space is the smallest segment and currently a money-loser. Revenue was $4.1B in 2025, up only 7.6%. It swung to a $657M operating loss (from a $21M profit in 2024). The reason is Starship. R&D in the segment jumped 64% to $3B as they poured money into the next vehicle, and in Q1 2026 alone Starship R&D was $930M. So the cash from launching satellites is being plowed straight into the next generation rocket that’s supposed to make the future vision achievable.

B. Connectivity

Connectivity represents the Starlink business, and it’s the segment that actually prints money.

As I mentioned above, it is only possible with the launch flywheel. Cheap, reusable, high-cadence launch is what lets you put up (and constantly replenish) a constellation of ~9,600 satellites in low-Earth orbit. No one else can deploy mass to orbit at that cost, which is why no one else has a constellation at this scale. The S-1 notes SpaceX has launched more than 80% of all mass to orbit globally each year since 2023.

The subscriber story of Starlink shows signs of a landgrab strategy. Starlink went from 2.3M subscribers (2023) to 4.4M (2024) to 8.9M (2025), and 10.3M by Q1 2026. Monthly ARPU fell the whole way: $99, then $91, then $81, and down to $66 in Q1 2026.

That ARPU decline is somewhat deliberate and represents both the push into lower-income countries and additional cheaper plans.

Overall, the financials of this segment are very strong. Connectivity did $11.4B in revenue in 2025, up 50%, with $4.4B in operating income. That’s a ~39% operating margin on a business growing 50%. Q1 2026 revenue was $3.3B, up 32%. Its a profitable, fast-growing, hard-to-replicate utility and has a big TAM ahead of it.

And Musk sums up the importance of Starlink to the overall company well:

C. AI

The AI segment is xAI, which was founded in 2023 and folded into SpaceX in early 2026 (the merger closed February 2). It houses Grok, the X platform, data licensing, and the compute infrastructure.

There are two things going on with this segment: the shift of the business from an ads business when X was bought to more of a subscriptions based business, and the additional revenue that comes from Grok (via API, etc) which is still relatively small compared to leading AI labs.

On the surface, it looks rough. “AI” revenue (which includes ads) was $3.2B in 2025, up only 22%, with a $6.4B operating loss as R&D rose 331% to $5B. In Q1 2026 it was worse on a growth basis: revenue of $818M, up just 12.5%, with a $2.5B operating loss, and ad revenue continued to fall in Q1. Below is a rough overview of the current state of the AI segment.

So if you stop at the income statement presented, the AI segment is a slow-growing, deeply unprofitable drag on the company. But that’s the picture before the recent deals which change things.

II. Recent developments in the AI segment

Two things happened in May 2026, right before the filing, that paints SpaceX in a somewhat different light.

The first is the Anthropic deal. SpaceX signed Cloud Services Agreements with Anthropic for compute capacity across its Colossus and Colossus II data centers. Anthropic agreed to pay $1.25B per month through May 2029, with capacity ramping at a reduced fee in May and June 2026. Either side can terminate on 90 days’ notice.

The entire AI segment did $3.2B in 2025. So this one contract, fully ramped at ~15B/yr, is roughly 5x the segment’s trailing revenue.

The second is the Cursor deal. In April 2026, SpaceX signed a compute and option agreement with Cursor. Under the compute agreement, SpaceX gives Cursor GPU capacity and they collaborate to improve Grok and potentially jointly develop new models. Under the option agreement, SpaceX has the right (not the obligation) to acquire Cursor outright at a $60B implied equity value, exercisable in a 30-day window after the IPO (or by September 30, 2026).

SpaceX frames coding as one of the best use cases for AI because it generates high-quality, verifiable data and constant inference demand. Cursor’s developer interaction data (prompts, iteration cycles, architecture decisions) feeds back into model training, including Grok. And if they exercise the option, Cursor becomes an owned application sitting on top of their own compute and own models.

If SpaceX terminates the option, Cursor is owed a $1.5B termination fee plus an $8.5B deferred services fee. So they’ve effectively pre-committed to either buying Cursor or paying a large breakup cost.

Put together, these deals give the AI segment a much clearer shape. Three layers that are compute, model/intelligence, and apps.

Compute is the base, and right now it’s the most valuable part. SpaceX built Colossus and is training Grok 5 on Colossus II. The interesting move is that they have shown willingness to lease the spare capacity. Anthropic is the first big tenant but there may be more.

Models is Grok, trained in-house, differentiated by real-time integration with X data. This is also where the Cursor collaboration sits, jointly developing models and feeding coding data back into Grok’s training.

Apps represents X and the Grok app today, and is the layer that the Cursor option can also bolster. If they exercise, Cursor becomes an owned coding app running on their own models and compute. They’re also building Macrohard with Tesla, an agentic platform meant to emulate digital workflows.

III. The financial picture

At the consolidated level, 2025 looked like this: $18.7B in revenue, a $2.6B loss from operations, and $6.6B in Adjusted EBITDA.

The capex split is quite stark, compared to the revenue split. Of the roughly $10B SpaceX spent in Q1 2026, about $1B went to Space, $1.3B to Connectivity, and $7.7B to AI. For the full year 2025, around 60% of capex went to AI.

The picture of spend and profitability relative to revenue growth isn’t great, which is why I think the Anthropic (and Cursor deals) are critical.

Annualize the Q1 2026 quarter and SpaceX is running at about $18.8B. Grow each segment off that base for the rest of the year and you conservatively get to roughly ~$22B run-rate by Q4.

Then layer in Anthropic and Cursor. Anthropic at the full $1.25B per month is $15B annualized. Cursor could generate another $3B-$4B in revenue (it’s at ~$3B today and growing). Stack those on the organic base and you land around a $40B to $41B run-rate exiting 2026, on a relatively conservative estimate of organic growth and not assuming more compute partners.

At least partially this helps ground the $1.75T valuation in some more reasonable sense. Compared to a ~20B run-rate business growing relatively slowly, it now looks like a ~40B+ run-rate business growing over 100% y/y albeit because of one compute deal. More importantly, it also shows Elon’s willingness to make sure that he monetizes his spare compute, even if internal products don’t take off which helps alleviate some of the concerns around the high Capex.

IV. Orbital compute and the space economy

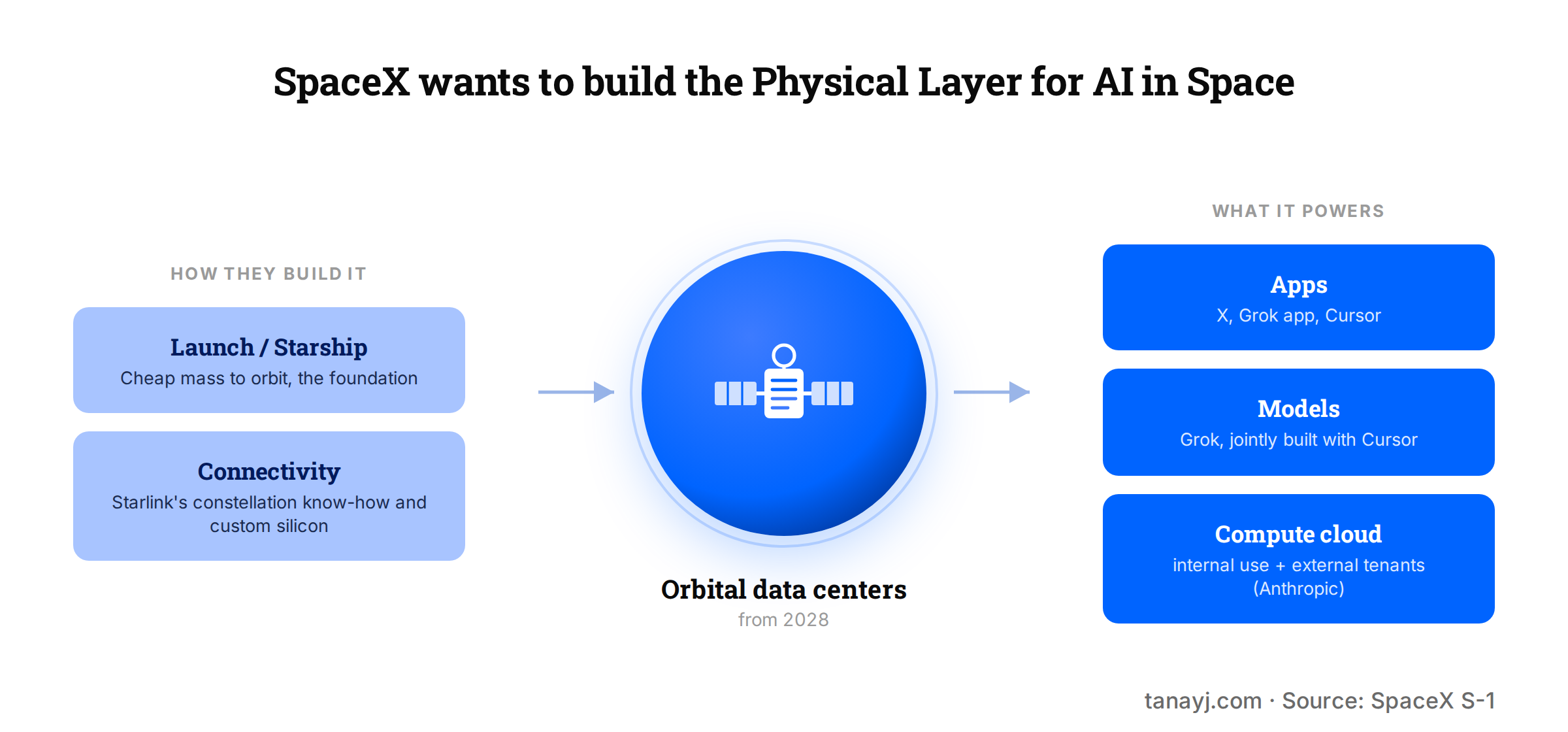

Despite the improving AI segment in the near term, it still looks bolted on to the Space and connectivity business. Orbital AI compute is where that changes and the reason these are all in one company becomes more clear.

One way to think about SpaceX may be less a rocket company with an AI business attached, and more of a physical infrastructure company for the AI age. The launch business lowers the cost of accessing orbit. Starlink proves SpaceX can operate distributed infrastructure in orbit at global scale. The AI segment creates the demand for compute. Orbital AI compute are where those three pieces converge.

What is orbital AI compute you may wonder? Satellite constellations that act as data centers in space, using solar energy for power and the space environment for cooling. SpaceX expects to start deploying these as early as 2028.

The launch (Space, Starship) segment allows SpaceX to put that much mass in orbit cheaply. The satellite expertise from Connectivity gives them some of the know-how to do so (and frankly helps fund some of it), because orbital compute is basically the Starlink playbook pointed at a different payload.

And the AI segment is what monetizes that compute, either by selling that compute or using it in models or application.

The bottleneck for terrestrial AI is power and cooling. In orbit you get abundant solar and free cooling, if you can get the mass up cheaply and move data back down. SpaceX is arguably the only entity on Earth today that can pull this off, given their Space segment and know-how from Starlink.

It is interesting that SpaceX’s own TAM slide puts it at $28.5 trillion, and $26.5 trillion of that is AI, highlighting how important the orbital data centers may be into unlocking the AI TAM (thought SpaceX still needs to work on the AI demand piece).

There’s also a bigger vision in the filing, which is that Starship in the future could be capable of landing massive cargo on the Moon which then opens up factories on the Moon could manufacture millions of AI compute satellites using lunar resources and deploy them farther into space. The future markets they list include space manufacturing, lunar and Martian energy production, and asteroid mining.

V. The Bet on Starship

SpaceX’s future vision all hinges on Starship. The filing even says so directly: the Space growth strategy “depends on the successful development of Starship at scale.”

Falcon is proven. Falcon 9 carries about 23 tons to LEO, has flown roughly 620 times with 99%+ success rate. Falcon Heavy carries about 64 tons. But it won’t allow SpaceX’s full ambitions. That requires Starship

Starship V3 is designed to put 100 tons into orbit fully reusably, with aircraft-like turnaround, and future versions aim to double that. This is important for two reasons:

Payload: you can’t deploy the next generation of hardware on Falcon. The new Starlink V3 satellites (1 Tbps of downlink each, versus the current generation) are designed to launch on Starship, starting in the second half of 2026, and the orbital compute satellites need that mass capacity too.

Cost: full reusability with rapid turnaround is what collapses the cost per kilogram to orbit, which is the input to every other ambition.

So what’s the current status you may wonder? They’ve run 11 flight tests so far, with a 12th scheduled that debuts the next-generation vehicle and Super Heavy booster. They’ve already pulled off the “chopstick” booster catch, where the launch tower’s arms catch the returning booster, which is what enables rapid reuse and eventually multiple launches per day. They expect Starship to begin delivering payloads to orbit in the second half of 2026.

The investment behind this is large and concentrated. Space-segment R&D was $3B in 2025, most of it Starship, and another $930M in Q1 2026 alone, and arguably makes the financials of the core business (ex AI) look worse than it is.

Every ambitious plan of the company runs through Starship. Starlink’s next-gen satellites need it now. Orbital compute needs it for cheap mass. The Moon and Mars plans are impossible without it.

VI. Musk’s pay package

I’ve mentioned a few times that SpaceX is unique and inspirational. Nothing makes the scale of their ambition more clear than Musk’s pay package.

Musk has two performance awards in there, which tell a lot.

The first, granted in January 2026, is 1 billion performance-based shares. Both of two conditions must be met for any tranche to vest. First, market-cap milestones across 15 tranches, running from $500B up to $7.5 trillion. Second, and I’m quoting the filing:

The Company’s establishment of a permanent human colony on Mars with at least one million inhabitants.

So even if SpaceX becomes the most valuable company on Earth, the full award doesn’t vest until there’s a city of a million people on Mars.

The second, granted in March 2026 was tied to xAI and is called the “AI CEO Award” Same two-part structure: market-cap milestones (12 tranches, $1.065 trillion to $6.565 trillion), plus a second condition which I quote again:

The Company’s completion of non-Earth-based data centers capable of delivering 100 terawatts of compute per year.

For reference, total US electricity generation capacity is roughly 1 terawatt. So the target written into the filing is space-based compute at something like 100x the entire US power grid.

It gives you a sense of the scale of SpaceX’s ambition. Musk gets additional shares if and only if the company becomes multiplanetary and/or builds compute off Earth.

Closing Thoughts

This has been a long piece and there’s a lot more one can say about SpaceX. But to summarize, the launch business is a strategic asset, which is increasingly mostly being used internally to power a strong Connectivity business which is growing fast at 10B+ in scale and very profitable, but is being used to power investment in R&D for Starship and the AI business. The AI business has shown its ability to build infrastructure, which they are now open to leasing, and are trying to build better models to compete at the model and application layers as well.

Any forecasts or analysis based on current or the end of 2026 run-rate will make it difficult to justify the ~1.75T valuation, but SpaceX is arguably the only company today that can help build the Space economy and all that that may entail from AI compute to mining materials to making us an interplanetary species. So how much value do you give to that? And to Elon Musk being Elon Musk.

In closing, here is a particularly profound segment you don’t see in most S-1s:

For the entirety of its existence, human civilization has lived on a single celestial body: Earth. The current paradigm, in which human civilization is confined to one planet, exposes humanity to existential threats that are unpredictable and uncontrollable on a planetary scale. By moving beyond the only home we have ever known, we ensure species-level redundancy and that the light of consciousness will not be tied to a single planet subject to the inevitable hazards of a harsh and vast universe. We do not want humans to have the same fate as dinosaurs.

If you have any comments or thoughts, feel free to tweet at me.

Interesting perspective, especially the idea that the different businesses make more sense when viewed as parts of the same long-term infrastructure strategy