Startups and Value Creation and Destruction

An Analysis of Public Company Valuations versus their Aggregate Capital Raise

Hi friends,

Hope everyone had a great labour day weekend!

With some of the fall-out from the macroeconomic changes on public tech companies, there has been a lot of discussion around capital efficiency and value creation. This week, I’ll be discussing value creation in the public tech company landscape a bit broadly, using a relatively straightforward measure: what the market cap / equity value of a company is today vs. how much money the company raised in equity to get there.

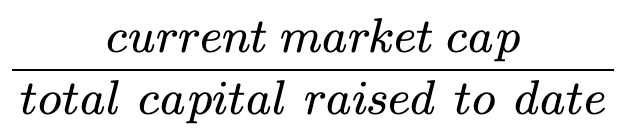

The market cap to equity raised ratio

There have been a lot of companies that sport quite significant market caps, but have not really created much value for their investors in aggregate if one looks a bit further. The reason for this is that they might have raised a lot of money to get to that market cap, and so in reality, their market cap might not tell the whole picture.

So one way to measure both capital efficiency at a high level, but also value creation more generally is to compare the market cap to the equity dollars raised.

For this analysis, I’ll be using the ratio of the two: current market cap / total equity raised to date.

I used data from Pitchbook and focused on public technology companies the majority of which are venture-backed1.

We can use the ratio to group companies at a high level based on capital efficiency/value creation2:

A ratio of under 1: A ratio of under 1 means that a company is worth less than the total $ it raised and so in some sense it has been value destructive.3

A ratio of 1-3x: While a ratio above 1 means that the company has in theory at least created value, it still doesn’t indicate that the company has been greatly efficient given the opportunity cost and time value of the dollars that was invested. For the purposes of segmenting further, I’ll use 1-3x as an okay level of value creation.

A ratio of 3-10x: A good level of value creation.

Greater than 10x: A great level of value creation where a business has been very capital efficient or been able to compound capital enough such that it doesn’t rely on outside capital beyond a certain point.

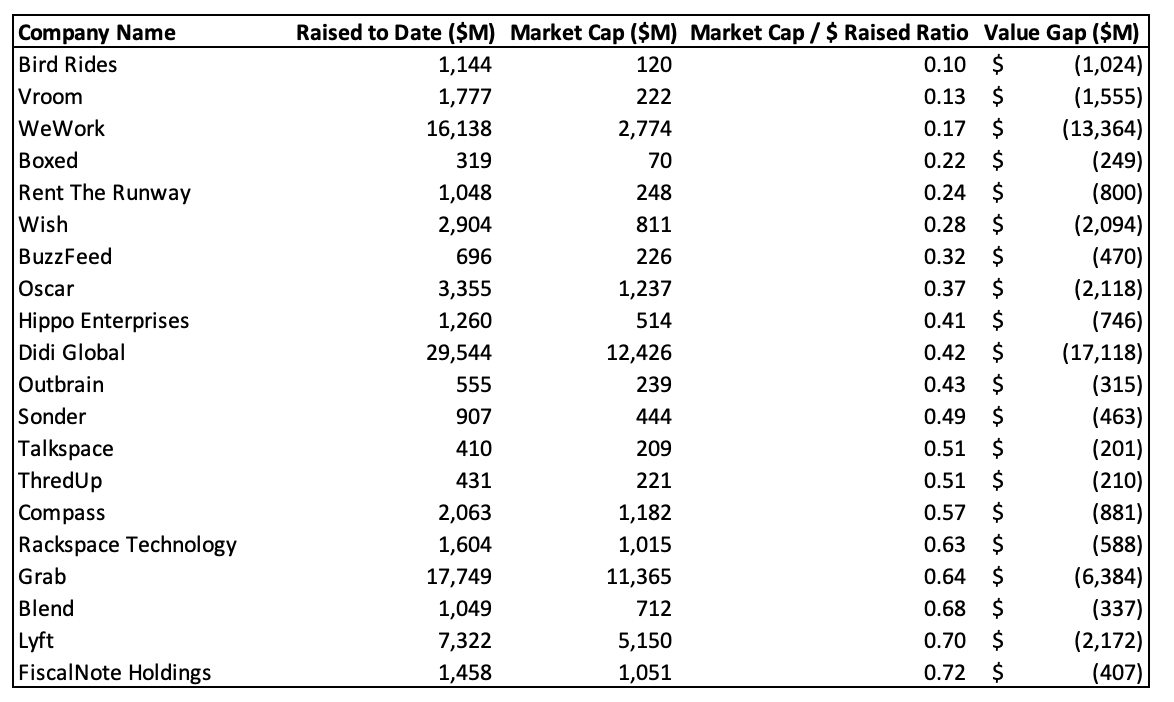

Ratio of <1x: Value Destroying Companies

Much has been written about a few well-known companies that “destroyed value” such as WeWork.

But many other relatively high-profile companies fall under the value destructive bucket when using the measure of a market cap to equity raised ratio of under 1, as illustrated below, including Lyft, Oscar, Grab, Sonder, Compass and others.

A couple of things stand out:

There aren’t too many pure software companies on the list. Most of them involve something in the physical world (real estate, ridesharing) or a regulated industry (fintech/lending, healthcare), or media. In some sense, perhaps that’s one of the benefits of the software. If it works, it usually works in a relatively capital-efficient way.

Customer Value doesn’t always translate to Shareholder value: Many of these companies created value for customers, but that didn’t translate into value for shareholders in aggregate. In general, the former doesn’t have to mean the latter since it’s possible all the value generated goes directly to the consumer as surplus.

Betting on wrong industries/market structure: It’s likely that a lot of shareholder value was “destroyed” because investors thought the economics of a certain type of business might look like software at scale, but over time it became clear you couldn’t escape the realities of the industry and/or the competition from the other well-funded competitors meant that the market structure didn’t play out as expected. For example, multiple ridesharing/transportation companies are on this list – Didi, Grab, Lyft and Bird. Notably, Uber isn’t.

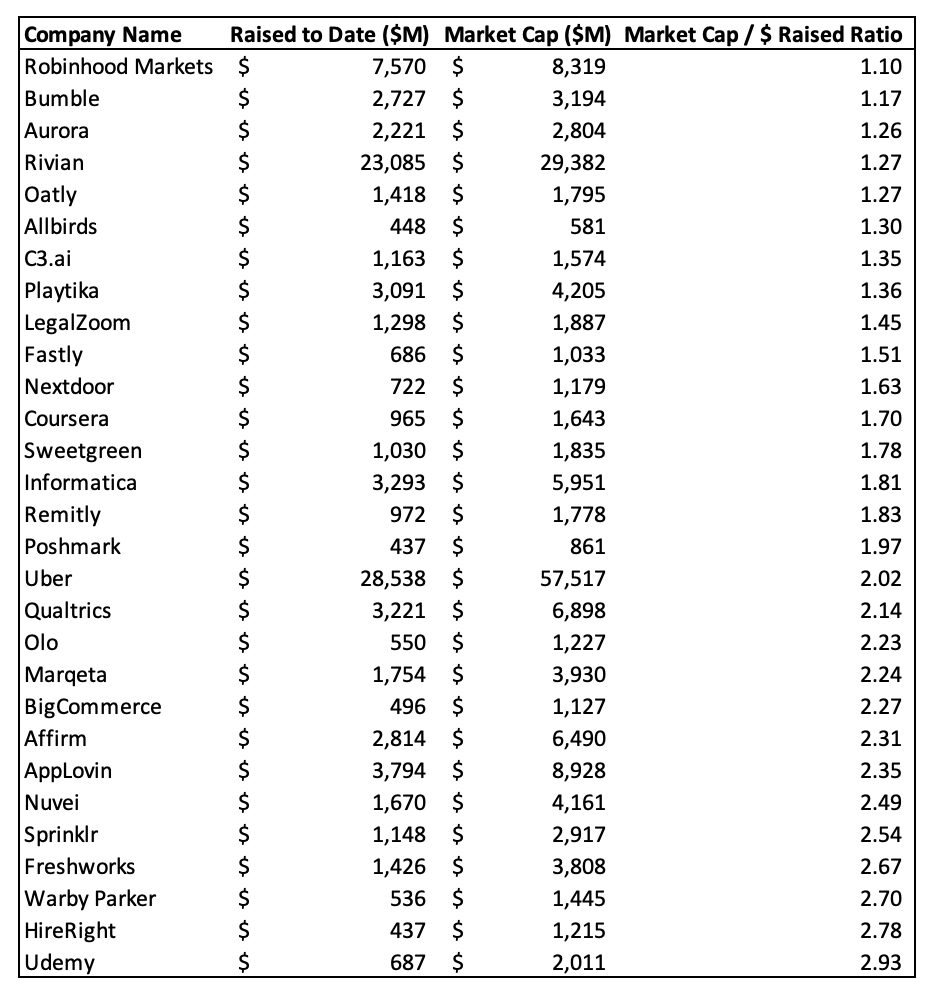

Ratio of 1-3X

A ratio of 1-3x isn’t bad per se, but it isn’t good either. Generally, many of these companies provided only a small positive risk-adjusted return in the aggregate when factoring in the time period.

Some illustrative companies that fall in this range are below:

A couple of observations:

DTC/Consumer Brands were only “okay” as a category: Many of the marquee DTC brands such as Allbirds and Warby Parker and venture-backed consumer brands such as Oatly are in this range affirming something that’s become well known over the last few years – that just because you sell online, that doesn’t suddenly make them “tech quality” businesses in terms of capital efficiency (and outcomes).

Uber, despite having struggled over the last few years, was the only real “winner” in rideshare from an aggregate equity value creation perspective.

Ratio of 3-10X

These companies have fared relatively well in terms of the value they’ve created relative to the amount of capital they’ve needed to raise.

Companies that fall in this bucket are below. As one can see, it includes a number of software names, and some of the more “successful” fintech, delivery and commerce plays such as NuBank, Doordash, and Coupang.

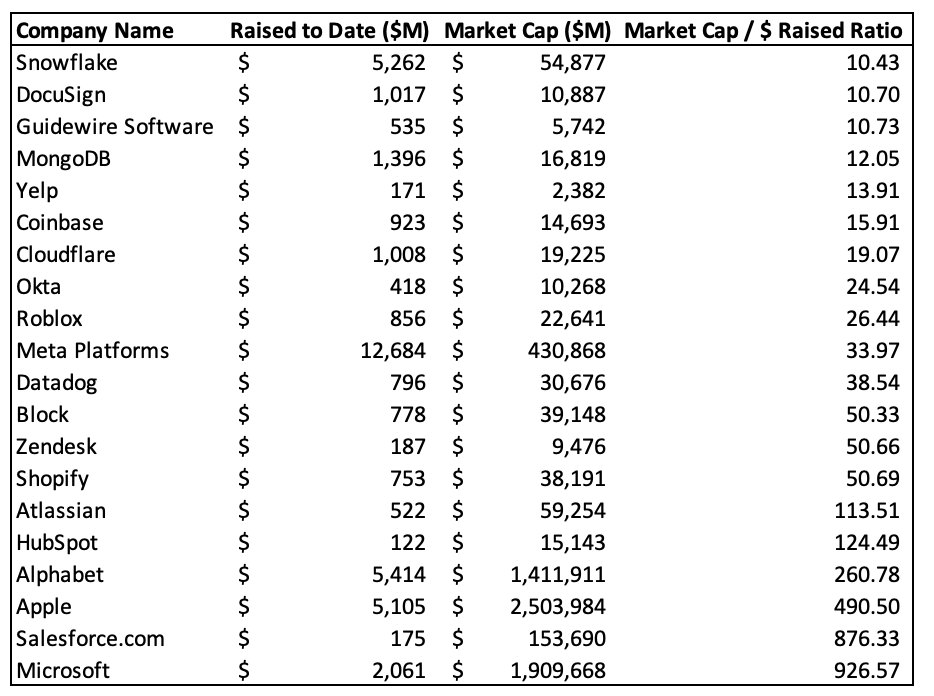

Ratio of 10X+

At a high level, all of these companies have been extremely value creative on the equity $ put in initially. The classic FAANGs fall into this bucket, but it should be noted that because they went public a while ago, they’ve essentially had more time to compound market cap and so I wouldn’t pay much attention to the actual ratios beyond a point or to compare companies. However, any company that falls in this category has not needed too much external capital and has been able to create a solid amount of value itself.

For a more apples-to-apples measure between these companies, one might want to look at something like Return on Incremental Capital.

Closing Thoughts

A couple of closing thoughts on this topic:

Large outcome does not mean Great outcome: Many companies such as DiDi, Grab, Rivian, and Robinhood sport close or above to decacorn valuations, but just raised so much money along the way that they weren’t necessarily a great outcome for all the investors in aggregate.

Value Destructive Companies may be good investments too, depending on the stage: While it is the case that for “value destructive companies” as above, investors in aggregate lost money, that doesn’t mean that they didn’t make good early-stage investments. In fact, in many of those cases, early investors were rewarded handsomely, and it was only the later stage and public market investors that lost out.

This is one high-level measure but by no means perfect, especially in the positive range: While this is a good rough measure for value creation relative to say venture type dollars raised, it doesn’t factor in the timing of dollars raised or the additional capital available to a business once they start to generate free cash flow, so is not very useful to analyze public companies against each other for investment purposes and is biased to companies that haven’t needed to raise money externally for a while. Other measures that can be used include ROIC (public companies), and ARR added/burn (SaaS).

Thanks for reading! If you liked this post, give it a heart up above to help others find it or share it with your friends.

If you have any comments or thoughts, feel free to tweet at me.

If you’re not a subscriber, you can subscribe for free below. I write about things related to technology and business once a week on Mondays.

Note that Pitchbook sometimes doesn’t do a great job of capturing public offerings post the IPO so the data may be inaccurate for a few companies.

The categories between 1-10x are for the purposes of illustrating the categories roughly, and I wouldn’t read too much between say an 9x and a 10x for example.

Or more precisely, based on the current market capitalization, the market’s expectation for its future performance is such that it has been value destructive.