Private Equity and SaaS Valuation Floors

The growth of LBOs of public SaaS companies

Welcome to the 65 people who have joined us since the last edition. If you’re reading this but haven’t subscribed, joined the 5,000+ other curious readers like yourself here:

Hi friends,

Happy Thanksgiving break to those who celebrate! Hope everyone has a great weekend.

Last time out I wrote about the largest leveraged buyout in history, Musk’s acquisition of Twitter. This week, I’ll discuss leveraged buyouts of another form: those of public SaaS companies by Private Equity firms.

Background

In recent months, we’ve seen public market SaaS valuations collapse (much like all other valuations), as in the chart below.

Median EV/next twelve month revenue multiples went from 10.9x pre-COVID to over 20x, and have since come crashing down to 4.9X, the lowest in 5 years.

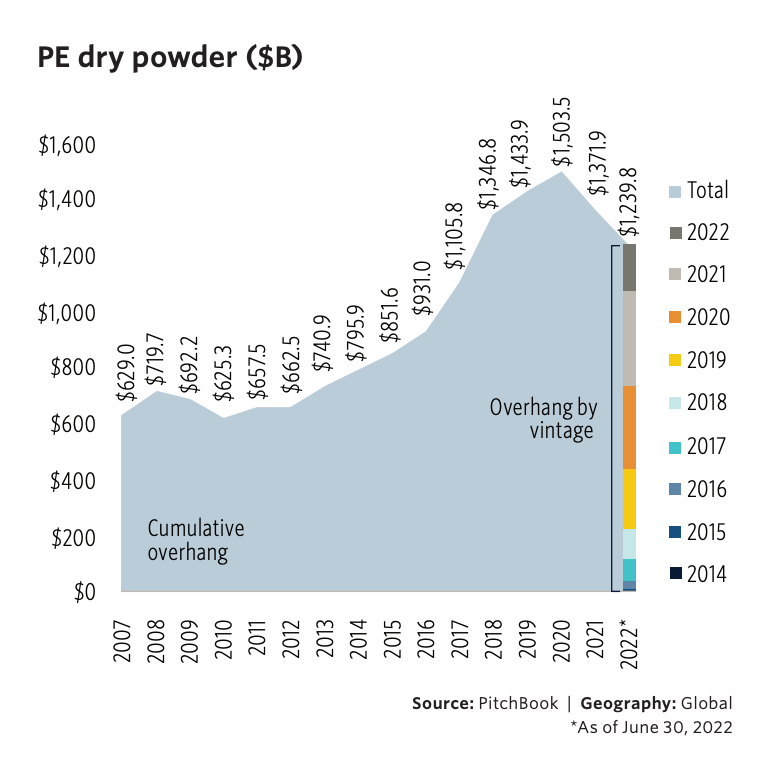

At the same time, there is over $1T of dry powder available in Private Equity, which is pretty much as high as it’s ever been prior to COVID.

Between the dry powder and the lower multiples, we are likely to an increase in the acquisitions of public SaaS companies by PE firms, especially the ones that have historically been buying tech businesses.

Private Equity and SaaS

PE Sources of Returns

While there are many different strategies and approaches, one of the most common private equity strategies is the leveraged buyout of companies, where the entire company is purchased, debt is put on it and the company is run and grown with the debt being paid down, and then eventually sold.

Returns on a typical investment usually come from 3 factors:

Revenue/Profit Growth – Since at the time of sale, the company typically has more revenue/profit than at the time of purchase, that results in a bigger sale price and drives returns

Leverage – Typically something like 20-25% of the purchase of a company may be financed with debt. This provides leverage and essentially increases the return to equity holders if things go right. Usually prior to the time of sale, the debt has been partially or fully reduced.

Multiple expansion — Most companies that PE acquires are done so on a multiple of EBITDA or EBIT. In SaaS however, many are unprofitable, and so the price paid can be considered as a multiple of revenue. Post acquisition, the revenue is often grown through both inorganic consolidation and organic growth, and the efficiency of the business is increased. Because of the larger size, as well as down to market timing of buying and selling, PE firms can benefit from selling a company at a higher multiple of revenue/profit than what they paid, and so it also drives returns.

As an example, let’s say a $100M ARR SaaS company is acquired by a PE firm at 5x revenue. The purchase price is $500M, but let’s say $100M is debt and $400M is equity.

At the time of the sale 7 years later, the company grows to $200M in revenue and is run more profitably is sold for 6x revenue. Let’s say no debt has been paid down. So the selling price is $1200M.

Now, the equity went from $400 to $1100, and the returns were driven by:

Revenue growth: Revenue doubled from $100M to $200M, implying a 2x return from this.

Multiple expansion: The selling multiple is 6x vs a 5x purchase multiple, implying a 1.2x return from an increase in the multiple

Leverage: One way to think about the value of leverage is that had there been no debt, then $500 of equity would have been needed, which would now been worth $1200. But instead, $400 of equity was needed which is now worth $1100. Therefore, leverage helped increase the return on equity from 2.4x to 2.75x, implying a multiple of 1.15x.

Why PE Likes SaaS

Given the above, why have PE firms liked SaaS assets, at least over the last decade or so? It’s for the same reasons that many other investors do and tied to their sources of returns above.

Recurring, Predictable Revenue: Many SaaS companies have >100% NDRs which means that there’s some element of revenue growth baked into the existing customer base. Given this predictable and recurring nature of revenue, it makes for a good investment both from a revenue growth perspective and from a putting leverage on the business perspective.

Capital Efficient: SaaS companies are generally capital light and produce strong free cash flow. This allows for putting more debt on the business and for growing the business without investing very heavily in capex.

Unprofitable: Given the unprofitable nature of many SaaS companies, there’s generally a belief that by taking them from unprofitable to profitable and improving the efficiency of them and paying low multiples on revenue in markets such as today where profits are prioritized, one can expand multiples.

Robert Smith, founder of Vista Equity Partners once said the below which highlights why Vista has been a fan of SaaS:

“Software contracts are better than first-lien debt. You realize a company will not pay the interest payment on their first lien until after they pay their software maintenance or subscription fee. We get paid our money first. Who has the better credit? He can’t run his business without our software.”

If you don’t yet receive Tanay's newsletter in your email inbox, please join the 5,000+ subscribers who do:

Deals in 2022

In 2021, PE firms made $29B worth of acquisitions of tech startups1. As we close in on 2022, the number is $65B for venture-backed software startups, more than double that of 2021.

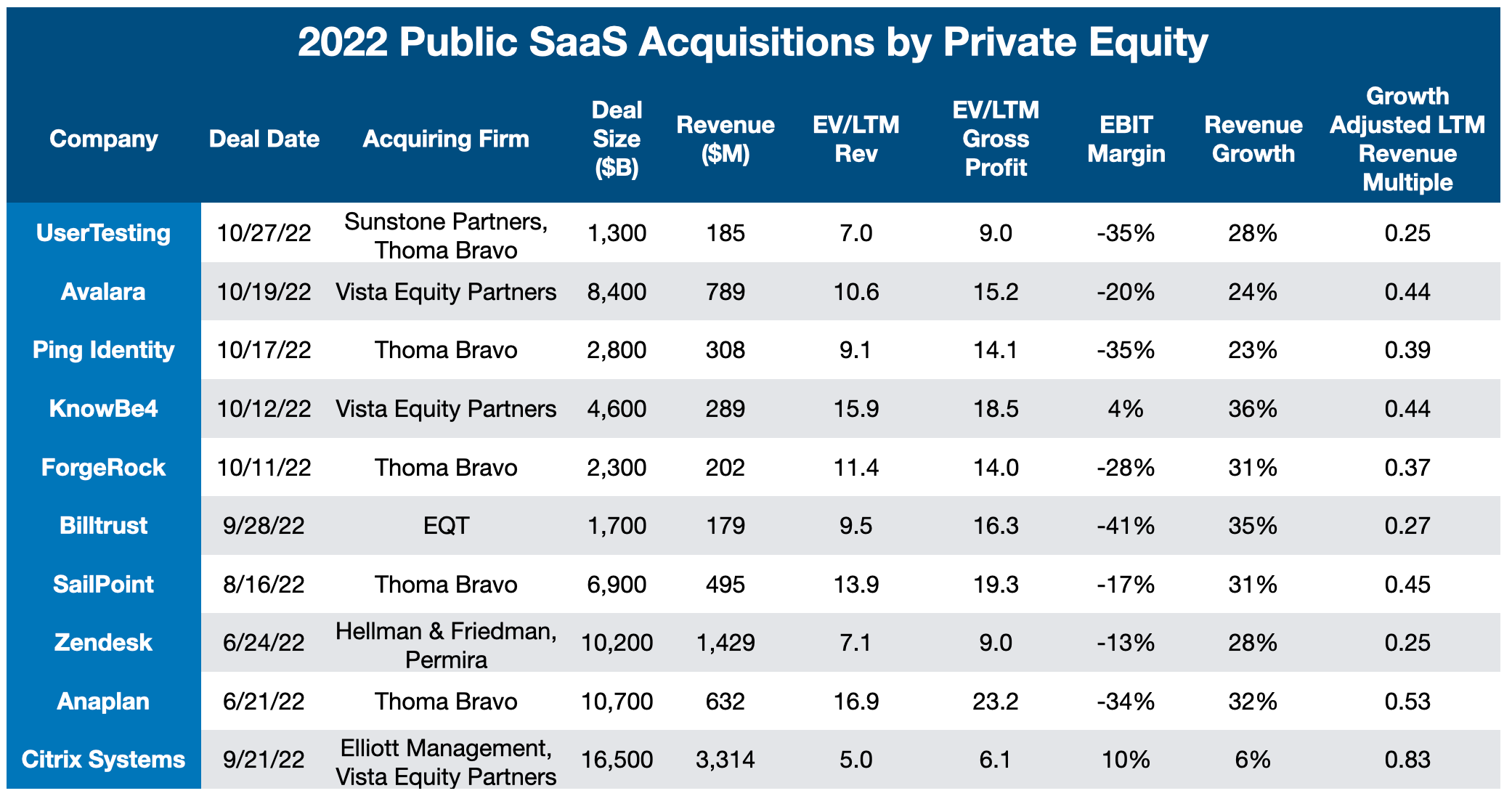

So far, we’ve seen ~10 public tech software companies acquired, with an increase over the last few months as multiples have started to compress.

No one knows whether we’ve hit a bottom yet, but the increase in PE buying indicates that they’re happy to pay a premium over these market multiples to buy up assets.

A few things stand out looking at the above:

While the right price is very dependent on the company and the opportunity and indeed the market environment, it seems that PE is generally willing to pay 5-6x next year’s revenue / 10-12x next year’s Gross Profit assuming 25-30% growth.

Typically, most of the companies being purchased are growing 25-35%, indicating that they do tend to have some more growth and room to run. However, so far at least the extreme high fly growers (50-60+%) haven’t been targets for acquisition, likely because of the multiples they will command.

Most of the companies acquired are still not profitable, at least on a GAAP basis. In some sense, that helps the PE playbook. Buy the companies that have scaled the business and been able to grow, but not profitably, and take them from their negative margins closer to their long-term potential margins, which are usually in the 20-30% range, while paying back debt and growing revenue at a reasonable rate.

Closing Thoughts

I suspect we’ll continue to see a high level of this kind of M&A in the coming years, especially if valuations in the public markets remain low.

And with the median multiples at 4.9x NTM revenue for SaaS companies, I wonder if the option of a potential PE exit puts somewhat of a floor on median SaaS valuations in the ~3-4x NTM revenue range (for the basket that has 75-80% median gross margins).

Even assuming a 20%-30% premium on the publicly traded price, it seems like PE would be pretty happy to gobble up assets growing at 20-30% at 4.5x NTM revenue.

Some of you might be wondering which companies may be prime targets for a potential PE acquisition or whether Elon’s running of Twitter will lead to some changes in the PE playbook. Both are worthy of discussion and I’ll save those for a future piece.

Thanks for reading! If you liked this post, give it a heart up above to help others find it or share it with your friends.

If you have any comments or thoughts, feel free to tweet at me.

If you’re not a subscriber, you can subscribe for free below. I write about things related to technology and business once a week on Mondays.

via Tom Tunguz

Great read👍