Observations from the Enterprise Tech 30 List

Hi friends,

I was going through the Enterprise Tech30 list earlier, so thought I would share some of my observations from the list in this week’s newsletter.

For those unfamiliar with the list, at a high level (detailed methodology), the list identifies the most promising enterprise tech startups by surveying over 95+ VCs, who picked 10 companies each by category (early, mid, late, giga), with the category cut-offs determined based on funding amounts raised.

With all that said, let’s get into a few of my observations from going through the list.

1/ The growth of developer tools and infrastructure

Almost 40% of the companies on the list are Developer infrastructure and tools, including companies such as LaunchDarkly, WorkOS, Linear, and others.

And it’s not a real surprise. There are likely somewhere around ~30M developers in the world. Given how important software is and continues to become, that number should likely be 2-3x that at least.

The immediate need given this developer shortage is to grow developer productivity, which can be increased in two broad ways:

Better tooling and infrastructure so developers can spend more time building

Better and more APIs so developers can spend their time building the core components that add value and leverage APIs and “reuse” the parts that are important but not the core competency of that company.

We see both types of companies on the list.

On the first point, there are companies such as Linear, Airplane, LaunchDarkly which make it easier to track issues, convert code to apps and launch features and overall allow developers to do their job better.

On the second, there are numerous companies across stages on the list which offers APIs to allow developers to abstract away elements in their software to companies focused on solving those specific problems, including Stytch (authentication), WorkOS (“enterprisification”), Stripe (payments) and Plaid (financial account linking).

2/ The rise of Low-code / No-code

One other way to address the developer shortage touched on above is to enable those not quite developers to be able to create software or software-like experiences whether it be for internal or external use or benefit from the infinite reusability and automatability of software for their workflows.

This rise of low-code and no-code is a clear trend observed on the Enterprise Tech30 list, with companies such as Zapier, n8n.io, and Retool all making the list.

Companies in this space provide a way for non-technical or semi-technical people to create internal apps or software or automate workflows which can automate or increase the efficiency of previously more manual or time-intensive workflows.

They also allow people to quickly build out an MVP of an idea to gauge market or investor interest, and in that way increase the surface area of what software exists or may exist.

And the quality of these tools has gotten surprisingly good over time. As no-code builder Bubble’s showcase demonstrates, people have built full-fledged marketplaces with authentication using basically 0 lines of code.

If you don’t yet receive Tanay's newsletter in your email inbox, please join the 4,000+ subscribers who do:

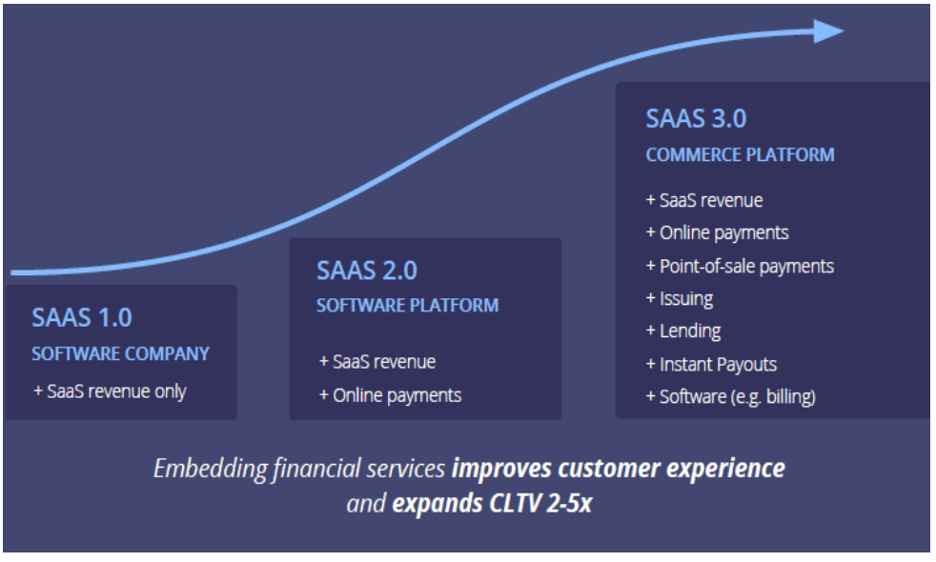

3/ Every SaaS Company Becomes a Fintech Company?

I’ve written in the past about the evolution of the SaaS model to embed payments and then various other fintech jobs to be done (lending, spending, etc).

In the Enterprise30 list, we see at least a few fintech infrastructure companies that can help enable this trend (Stripe, Plaid, Modern Treasury), which make it easier for other SaaS companies to interact with payments or move money around or with customers financial accounts.

In addition, in a lot of the ones on the “Giga” list, including Carta, ServiceTitan, Faire, TripActions, Brex, we see companies that may have started primarily with a SaaS or marketplace model, and are either already processing payments, issuing cards, providing lending or are likely to do so soon.

4/ Product-led Growth as the new default

Switching gears from category trends to business and GTM models, one thing that jumps out is that almost ~80% of the companies on the Enterprise Tech 30 list employ product-led growth.

A full discussion of product-led growth can be a separate post in itself, but the basic premise is that these companies typically have a self-serve (typically free) product tier which can be adopted by one or a few members of a team within an organization themselves to trial and gauge the value of the product, before upgrading (again in a self-serve manner) to the paid version.

Companies that are “product-led” tend to focus more of their resources on R&D and their product than sales (at least in the early days), and use the product as a way of acquiring and retaining customers.

As the end users of software in organizations seem to have more power around the decision making of products (rather than the typical top-down sales where the buyer might be different from the user), and the general bar for software in the workplace going up as people get more accustomed to delightful software across all aspects of their life, product led-growth seems to be the default approach these days for companies building applications, evidenced by the ET30 list.

Two points to note on PLG. If PLG is the “default” it isn’t really a differentiator for a startup these days, unless the company happens to be going after a vertical which is years behind. The second is that product-led doesn’t mean a company can get away without a sales force or “doesn’t need sales”. Over time, most PLG companies have to add a salesforce to continue to grow and convert team-based users into a broader deployment within an organization. However, the approach to selling can be different given that you can first start trying to go wall-to-wall in companies where some people already use the product.

Since PLG seems to be the new default, many more products are likely to emerge specifically targeting the sales motion best fitted for these companies. One example is Heads Up, which provides software for Product Led Sales teams to identify who to target given the rich data available about existing usage.

5/ Funding and Valuations

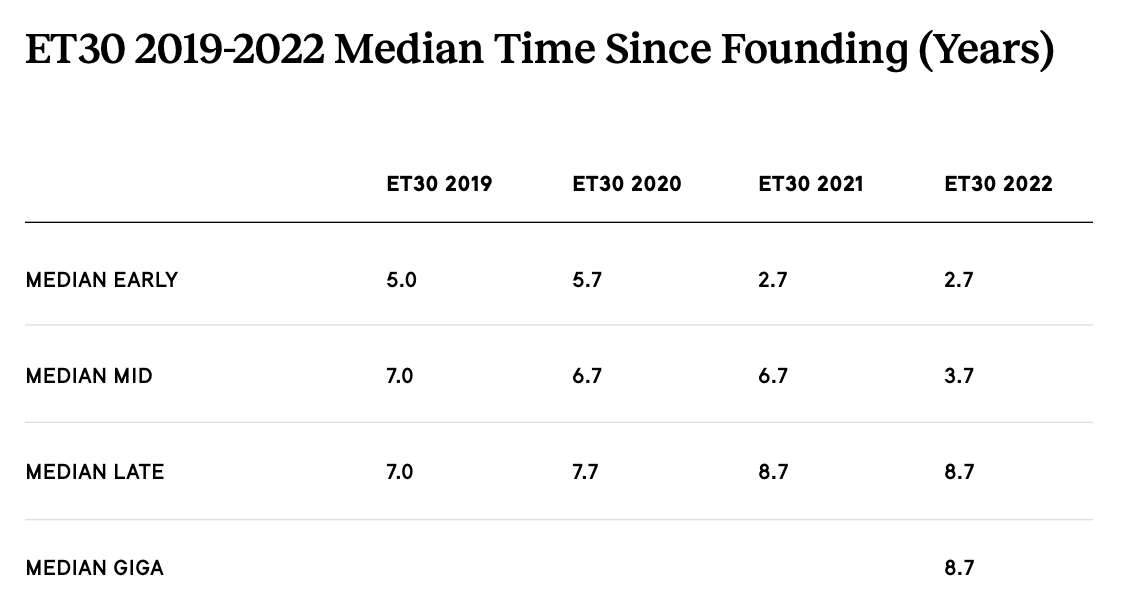

One last observation is around the speed, amounts and valuations at which companies are raising money. As the below set of charts show, the valuation of companies in most of these stages has gone up significantly. Similarly, the average age of the early and mid-stage companies has gone down significantly (meaning new ones are scaling more quickly, in terms of funding at least, and graduating to the “late” category more quickly).

It highlights how much more money companies are raising more quickly, and how valuations and multiples are higher than basically ever before.

However, over the past few months we’ve seen given public markets down ~50% for SaaS companies. Since many private companies haven’t raised since then, the above valuations, especially for the later stage companies, may not be reflective of the new environment, and they may face rounds at lower multiples (or even down rounds) on their next fundraise.

We’ve already seen companies such as dbt say they voluntarily lowered the valuation of their most recent raise (~$6B→$4.2B) to better reflect the realities of the market (and be more attractive to future employees).

Thanks for reading! If you liked this post, give it a heart up above to help others find it or share it with your friends.

If you have any comments or thoughts, feel free to tweet at me.

If you’re not a subscriber, you can subscribe below. I write about things related to technology and business once a week on Mondays.