Observations from the 2023 Enterprise Tech 30

This is a weekly newsletter about the business of the technology industry. To receive Tanay’s Newsletter in your inbox, subscribe here for free:

Hi friends,

This week, I’ll be sharing some observations from the 2023 Enterprise Tech 30, which we at Wing published the week before last.

For those unfamiliar with the list, at a high level (detailed methodology), the list identifies the most promising enterprise tech startups by surveying ~100 VCs, who picked 10 companies each by category (early, mid, late, giga), with the category cut-offs determined based on funding amounts raised. This year was the 5th edition of the list.

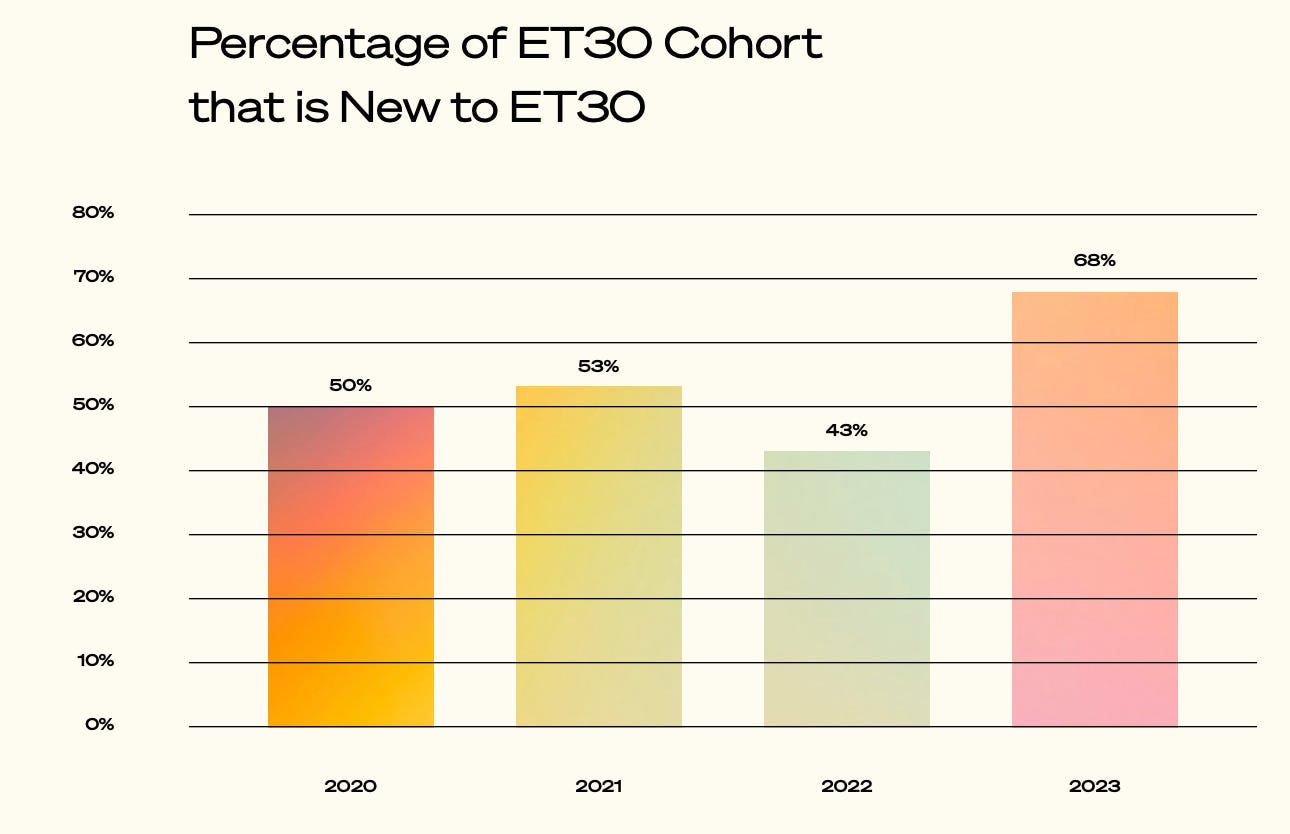

1/ Macro + AI creating opportunities and turnover

This year, 27 of the 40 companies were new to the list, the highest percentage since the list began.

This can largely be attributed to two factors:

The rise of generative AI and AI more broadly, with 10 of the new companies being critical parts of the movement, such as OpenAI, Pinecone, Langchain, etc.

A shifting macro underscored which more mature companies were well positioned for the bundling and budget cuts vs. which decelerated more strongly in this environment.

This year, five of the companies that made the list were founded within the last 18 months, which is a record high and speaks to how quickly things have happened.

2/ The rise of Generative AI

It’s hard to understate just how quickly Generative AI took things by storm. Its been under a year since the movement truly kicked off, and out of the 40 companies, almost half of them (~19 out of 40) either are:

building key infra powering the movement (OpenAI, Pinecone, Dust, Replicate)

AI-native applications (Jasper, Copy.ai)

or had launched significant product features that leverage foundation models (e.g. Hex, Airtable, Canva, Notion)

The third bullet also underscores how quickly “incumbent” products are adopting this technology — many of the products have integrated key features that leverage this technology within 6 months into the product, in a way that at least initially defends them from an AI-powered startup entrant.

3/ Product-led growth as the norm

This year, 30 of the 40 companies on the list employed a product-led growth model as a core motion (at least initially).

At a high level, that means that they had a self-serve typically freemium offering from early on targeting the end-users, and then over time will layer or already layered on a sales model to that motion.

Of the 30 companies, ~2/3rd had a technical user (developer/data scientist) as their end user (of which many were open source), and the rest focused on a business user, highlighting that the motion is applicable to all kinds of users.

There are many good reasons to not begin as a product-led company, such as:

If selling to certain functions/departments where people cannot bring their own tools (compliance, etc)

If the product needs a lot of integrations (data or other connectors) or services work to function properly

If the product only works when a large number of people in an organization are using it (multiplayer mode).

However, in other cases, it is worth it for companies to think through what a self-serve version of their product that provides some single-player value might look like before ruling out the PLG approach.

4. Cooling Valuations but only slightly

Looking at the median valuations of companies that made the list this year, they are typically 20-30% lower by category than in the previous year.

This is not too surprising given the shifting macro and multiples being down over 50%+, and in fact maybe the decline is lower than expected because this set of companies has been fueled by AI and so less affected.

On the same note, it is interesting that looking at the full universe of ET30 companies at the time they raised their seed, the valuations were relatively stable and still at record highs until late last year.

In addition, companies that eventually made it to the ET30 consistently raised at higher median pre-money valuations than ones that didn’t (chart below), at least suggesting that on average these companies tended to be “hotter” out of the gate.

Thanks for reading! If you liked this post, give it a heart up above to help others find it or share it with your friends.

If you have any comments or thoughts, feel free to tweet at me.

If you’re not a subscriber, you can subscribe for free below. I write about things related to technology and business once a week on Mondays.